Why is prepaid insurance a short term asset?

Prepaid insurance is often touted as a great investment by those who don’t know much about investing, but it’s more of a short-term asset than anything else. For the typical investor looking to boost portfolio, purchasing a prepaid health insurance policy is certainly not the wisest choice.

Despite what many prepaid insurance plans may tell you, they are not a long term asset. If you have a prepaid plan, chances are you have a medical condition, or you want to save for a vacation or home renovation. This type of coverage is fairly new. It was introduced in the early 2000’s and it went from $5 a month to $100 a month, so it’s only natural that you would want to keep it as a long term investment. After all, having insurance doesn’t make you a less likely candidate for medical bankruptcy.

Accounting Home Why is prepaid insurance a short-term investment?

17. September 2020

Accounting Adam Hill

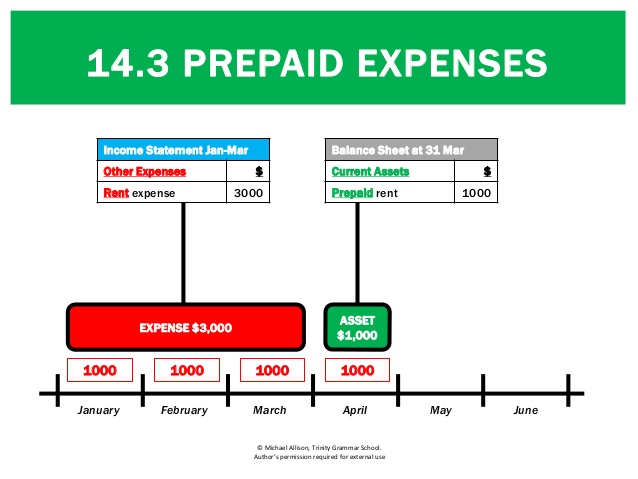

Prepaid rent expense exists as an asset account reflecting the amount of rent prepaid by the company. Once prepaid rent is recorded in the general ledger, the entity must make an adjustment to reflect the amount of rent used in a given period. Rent is the amount paid for the use of property that the company does not own, as explained on the Internal Revenue Service website. The calculation of the prepaid service charge depends on the amount of the monthly rent for the business. A company that z. B. prepaid $12,000 for one year’s rent, must credit cash in the amount of $12,000 and write off prepaid rent in the same amount.

Although some accounting systems can automate the amortization of prepayments, an analysis of the accounts must be performed each accounting period. For example, a business that pays $1,000 per month in rent should add $1,000 per month to the prepaid rent account beginning on the 30th month. September credit $9,000. That means the company has three months or $3,000 in prepaid rent left.

The expense is recorded in the income statement, and a $10,000 reduction in prepaid rent reduces the asset on the balance sheet by $10,000. Booking prepaid rent doesn’t have to be complicated, but it does require special attention at the end of the month. In the basic general ledger system, the bookkeeper posts the prepaid asset to the balance sheet account. This may require an adjusting entry to reclassify service costs against advances. Then a monthly entry is made to reduce the deferred expense account to reflect the lease costs.

Prepaid expenses are a type of asset on the balance sheet that arise because a company makes advance payments for goods or services that it will receive in the future. Deferred charges are initially recorded as an asset but are expensed over time. Unlike ordinary expenses, an entity obtains some value from deferred expenses over several accounting periods. For example, suppose ABC buys insurance for the next twelve months. ABC Company initially records the entire $120,000 as a debit to the prepaid insurance account, an asset on the balance sheet, and a credit to the cash account.

Calculation of prepaid rent costs

Therefore, it should be treated as an accrual and recognized over the full 12 months. If the premises rented are used for the production of goods, the rent is part of the value of the goods produced. To make the first journal entry for prepaid expenses, debit the prepaid expense account.

However, the adjustment for deferred charges affects both the income statement and the balance sheet of the entity. The January 31 adjustment results in an expense of $10,000 (rent expense) and a reduction in assets of $10,000 (prepaid rent).

What are prepaid expenses?

Each month, an adjusting entry is made to record $10,000 (1/12th of the prepaid amount) on the income statement as a credit of prepaid insurance and a debit of insurance expense. In the twelfth month, the last $10,000 is fully debited and the prepayment account is reset to zero. Generally accepted accounting principles (GAAP) require that the expense be recognized in the same accounting period in which the benefit of the related asset is received. For example, if an enterprise leases a large Xerox device for 12 months, it benefits from its use for the entire period. Accounting for the prepayment of the lease in the first month as an expense would not adequately relate the expense to the income from the use.

- Prepaid rent expense exists as an asset account reflecting the amount of rent prepaid by the company.

Since the prepayment is for six months, the total cost should be divided by six ($9,000 / 6). DateAccountNotesShouldCreditX/X/XXXXExpenditureXPrepaidExpenditureXLSay you prepaid six months’ rent, which amounts to $6,000.

Accounting for prepaid rent

Prepaid expenses are recorded in the books at the end of the accounting period to reflect the actual figures of the company. Rent is the amount of money that a natural or legal person, as a tenant, pays at regular intervals, for example. B. every month or quarter, the owner pays. When a tenant pays rent, the bookkeeper debits the office rent expense account and credits the cash account.

If you prepay the rent, you must record the entire $6,000 as an asset on your balance sheet. Each month you reduce the investment account by the amount you use. You reduce the asset account by $1,000 ($6,000 / 6 months) and record an expense of $1,000. The benefit of the costs incurred will be carried forward to the next reporting period.

Is prepaid rent a current or a non-current asset?

The first journal entry for prepaid rent is a debit for prepaid rent and a credit for cash. Both accounts are asset accounts and do not increase or decrease the company’s balance sheet. Remember that accruals are considered assets because they provide future economic benefits to the company.

Crediting an account reduces your cash or checking account. Non-current assets are long-term investments of the Company, the total value of which will not be realized in the current year. Examples of fixed assets are investments in other entities, intellectual property (e.g. patents) and tangible fixed assets.

Each month a rent payment is credited to the prepaid rent account and the service charge account is debited. This process is repeated as many times as necessary to record the cost of the service in the appropriate reporting period. The first journal entry for prepaid rent is a debit for prepaid rent and a credit for cash.

Both accounts are asset accounts and do not increase or decrease the company’s balance sheet. Remember that expenses payable are considered assets because they provide future economic benefits to the business.

This account is an asset account and the asset is increased by the debit. Deposit the money into the correct account that you used for payment, for example. B. a cash or checking account.

Is prepaid rent income?

Prepaid rent is rent paid before the start of the rental period to which it relates and therefore the lessee is obliged to recognise the amount of rent paid that has not yet been used. Rent is usually paid in advance and is due on the first day of the month for which rent is due.

Crediting the prepaid rent expense account decreases the account and debiting the prepaid rent expense account increases the account. Note that in each transaction, each debit entry has a corresponding credit entry for the same amount. DateAccountInvoicesDirect DebitCreditX/X/XX/XXXExpenses Paid9000Cash9000Add the invoices during the month based on the rental amount you are using.

At the end of each reference period, a statement of expenditure incurred during that period shall be entered in the appropriate register. This journal entry credits the prepaid assets account in the balance sheet, for example prepaid insurance, and debits the expense account in the income statement, for example prepaid insurance. B. Insurance Costs. When a payment is made that represents a prepaid expense, a prepaid expense account, such as. B. a prepaid insurance account, debited, and a cash account, credited. The prepayment is recognised as an asset in the balance sheet. A depreciation schedule shall also be adopted that reflects the actual consumption of the asset in future periods.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”Why are Prepaids assets?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Prepaids are assets because they are money that you have paid for in advance.”}},{“@type”:”Question”,”name”:”Is prepaid insurance expense or asset?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A prepaid insurance expense is an asset.”}},{“@type”:”Question”,”name”:”Is a prepaid expense a noncurrent asset?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” No. Prepaid expenses are a current asset.”}}]}

Frequently Asked Questions

Why are Prepaids assets?

Prepaids are assets because they are money that you have paid for in advance.

Is prepaid insurance expense or asset?

A prepaid insurance expense is an asset.

Is a prepaid expense a noncurrent asset?

No. Prepaid expenses are a current asset.

Unlock Your Coolest Summer Yet: Dive Into Quality Self-Care Trends

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

Creating Magic Chord D’Paspor Saat Bersamamu A Musical Exploration

Unveiling the Mystery: Exploring and Debunking the Myths of 101 Arti Kedutan

Industry-Specific Crisis Communications: How PR Firms Tailor Strategies

The Impact of Working from Home on Work-Life Balance

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home