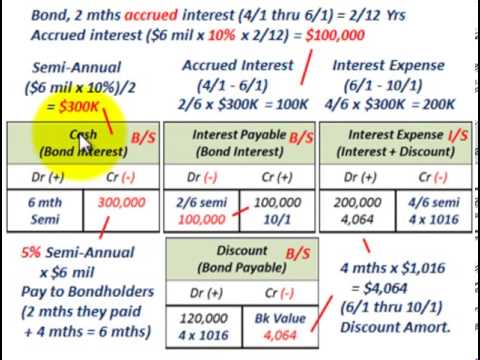

Amortization

Sometimes, a loan is just a loan; but sometimes it’s more than that. Sometimes, you are paying back the money you borrowed, and sometimes you are sending a check. It’s not always easy to know the difference, but some people have an even harder time knowing when the loan is fully paid off. If you want to be able to tell at a glance when it’s all said and done, then you need to know about amortization.

You may have heard the term, but what exactly is it and how can it cut your loan payments in half? Amortization is the practice of paying off a loan over time, usually over several years. This can help pay off your loan more quickly, or help you pay off your loan earlier.

Amortization is a type of mortgage financing that allows the amount of a mortgage loan to be paid down over time, by reducing the interest portion of each payment. Most debt is fully amortized over a long period of time.. Read more about amortization formula and let us know what you think. Depreciation of domestic accounts

22. May 2020

Accounting Adam Hill

Repayment is the process by which a loan (such as a home or car loan) is broken down into a series of fixed payments. Although each monthly payment remains the same, the payment is made up of parts that change over time. A portion of each payment is used to pay the interest (what your lenders paid for the loan) and to reduce the balance of the loan (also called repayment). Repayment is the process by which a debt is paid off over time through regular payments of interest and principal, sufficient to repay the loan in full at maturity. When paying a mortgage and a car loan, a larger portion of the fixed monthly payment is initially spent on interest payments.

However, a different system is needed for intangible assets, as there are no physical objects that can be written off. This is where depreciation comes in, a process that allows companies to record the cost of an intangible asset in increments so that further deductions can be made. Depreciation accounts are accounts in which companies book the amounts that are periodically depreciated. Your final installment will pay off the last balance of your debt.

To reflect the amortization of insurance costs, the entity must debit the general and administrative expense account and credit the deferred expense account with the amount of the amortization recorded. This entry reduces the company’s asset balance and increases its expenses. If it is determined that the amount is the same each month and the policy is valid for one year, an entry is made for 1/12 of the policy value.

The Company determines the useful life of an asset and divides the purchase price by the number of accounting periods in which the asset is expected to be used. Example: A company buys a patent for $120,000 and defines the useful life as 10 years. The annual depreciation expense would be $12,000, or $1,000 per month if you book depreciation expense on a monthly basis. Depreciation expense is an account that affects the income statement.

A company’s accounting system must record the purchase of an asset before depreciation can be recorded. The value of the asset is recorded in the balance sheet account with an account counterpart reflecting the nature of the payment, for example. B. Cash or bills that need to be paid.

Depreciation is the process of gradually allocating the cost of an asset over its estimated useful life to its expenses, thereby transferring the asset from the balance sheet to the income statement. It essentially reflects the consumption of an intangible asset over its useful life. Depreciation is usually used to write off the cost of intangible assets with a limited useful life. Examples of intangible assets are patents, copyrights, tax licenses and trademarks.

Impairment is strictly limited to assets that can only be used for a specific period of time. Companies use depreciation of physical assets, such as. B. Buildings and equipment to spread the cost of assets over time so that expenses can be deducted while the assets are in use.

This concept is also applied to items such as discounted bills of exchange receivable and deferred payments. A large part of accounting is to match expenses with revenues in the accounting period in which they are incurred. Therefore, different accounting policies allow estimating the amount that will be expensed or charged to revenue.

An entity recognises the value of an intangible asset only if it obtains it from another party and if the asset has a finite useful life. The Company transfers a portion of the cost of the balance sheet asset to the income statement each reporting period.

The amount of principal due in a given month is the total monthly payment (fixed amount) less the interest payment for that month. The following month, the loan balance is calculated as the previous month’s balance minus the last payment on the principal debt. The interest payment is recalculated on the new outstanding balance until all principal payments have been made and the loan balance at maturity is zero. The amortization period for the various intangible assets varies widely, from a few years to 40 years.

- Amortization is an accounting method in which the carrying amount of a loan or an intangible asset is periodically reduced over a period of time.

- A repayment schedule is used to determine the current balance of a loan, such as a mortgage or car loan, by making payments in installments.

Depreciation costs

This accounting treatment is required by the matching principle, which prescribes that the expense must be recognised in the period in which the benefit is realised. Intangible assets are defined as assets that do not have a material existence, but provide a long-term benefit to the company. Depreciation is typically applied to the purchase of trademarks, patents, copyrights, licenses and contracts – assets that provide tangible benefits to a business, but only for a specified period of time.

Why is depreciation important?

The accumulated depreciation balance is used as an offsetting account that is discharged by the asset being depreciated. In accounting, amortization of intangible assets means spreading the value of an intangible asset over time.

Determination of loan payment

It does this instead of booking the full cost at the time of purchase. Amortization is an accounting term that refers to the process of spreading the cost of an intangible asset over a period of time. Depreciation and amortization are non-cash expenses in the company’s income statement. Depreciation is the cost associated with the use of fixed assets on the balance sheet over time and amortization is the similar cost associated with the use of intangible assets such as. B. Goodwill, over time.

For example, amortization of goodwill for tax purposes is common with a 15-year period, but when it comes to financial reporting, goodwill is not amortized. Goodwill is the amount that should be paid in excess of the apparent market value of the business in an acquisition. Amortization is the process by which the cost of using intangible assets is amortized over time, as opposed to recording the cost only in the year of acquisition. In many cases, when a company acquires something, the amount spent is immediately used to reduce revenue.

Accumulated depreciation

As with depreciation of property, plant and equipment, entities use depreciation to allocate the cost of an intangible asset with a fixed useful life over the life of the asset. This method of recovering capital for a company is very similar to the straight-line depreciation method applied to tangible assets. An alternative would be to absorb the entire cost of the asset in one accounting period, which would make the profit for the period appear lower and violate the concept of reconciling costs and revenues.

When an asset is depreciated, its cost is divided by its useful life, and this amount is used to reduce the company’s income over several years. Useful life is a term used to indicate how long a good can be used before it is consumed. Depreciation is a sound accounting principle that reflects economic reality. Just as the benefits of long-lived assets, such as intangible assets, last for many years, the costs associated with acquiring the asset must also be allocated over the same period.

What is depreciation? Definition and examples

For example, in exactly 30 years (or 360 monthly payments), you pay off a 30-year mortgage. Repayment schedules help you understand how a loan works and can help you predict the balance owed or interest charges at any point in the future. For monthly payments, the interest payment is calculated by multiplying the interest rate by the loan balance and dividing it by twelve.

In general, an asset should be depreciated over its estimated useful life or, in the case of a bond or loan, over its term to maturity. If an intangible asset has an indefinite useful life, such as goodwill, it is not amortized.

Amortization is an accounting method that periodically reduces the carrying amount of a loan or an intangible asset over a period of time. First, repayment is used in the repayment of debts through regular payments of principal and interest over time. A repayment schedule is used to determine the current balance of a loan, such as a mortgage or car loan, by making payments in installments. Second, depreciation may also represent the allocation of capital costs related to intangible assets over a period of time, usually the useful life of the asset, for accounting and tax purposes.

Start-up costs can also be amortized, but generally, like other intangible assets, they cannot be amortized for more than 15 years. Some intangible assets benefit the company indefinitely but cannot be amortized.

What is an example of depreciation?

Depreciation expense is the amortization of an intangible asset over its expected useful life, which reflects the consumption of the asset. Depreciation expense is recorded by debiting the Depreciation expense account and crediting the Accumulated Depreciation account.Amortization is the most common calculation used to determine how much of a mortgage payment is paid off each month. Amortization of a mortgage is the amount of time, in years, that it takes to pay off the principal portion of the mortgage. Amortization is also referred to as amortization schedule.. Read more about amortization period and let us know what you think.

Finding Balance and Peace with Childcare Solutions

Moving Container from PODS: Unlock the Power of Portable Storage Units – Must-Know Uses

Assessment of Workiz HVAC Management Software: Features and Tools

Unlock Success: 5 Key Skills Every Stock Trader Needs

Could Cryptocurrency Benefit Your Finances?

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

Gemstone Holdings – Offering a Gateway to Numerous Trading Opportunities

The Adventure in Fajar Pakong 88: A Comprehensive User Guide

Revolutionizing Gaming: The Rise and Impact of Albumslot

Key Considerations for a Successful Manufacturing Business in Saudi Arabia

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home