Which Transactions Affect Retained Earnings?

A company’s income statement represents the flow of income that provides the basis for its assets and equity. The statement presents information concerning the business’s actual transactions that have taken place during a specific period of time. This statement is useful for a company’s financial health by showing whether it is making a profit or a loss. The income statement is prepared at the end of every period, and its main purpose is to inform the reader about the sources of income for the company and where the company’s money is flowing.

I recently learned that companies often have to account for transactions that are not reported in their financial statements. This can include backdated transactions or transactions where the CEO’s salary was not properly taken into account. Such transactions may have an impact on the company’s retained earnings.

Accounting Home Which transactions affect retained earnings?

20. May 2020

Accounting Adam Hill

![]()

The capital reserve does not directly increase retained earnings, but it can lead to a higher ROE in the long run. Share premiums represent the amount of share capital resulting from the sale of shares on the primary market above their par value. The par value of a share is the minimum value of each share as determined by the Company at the time of issuance. If a share is issued with a par value of $1 but sold for $30, the additional capital for that share is $29. In this scenario, you still own 1,000 shares with a face value of $10 each.

Preferred shares sometimes have a more than negligible par value, but most common shares today have a par value of just a few cents. In this context, the capital reserve is usually primarily an indicator of total paid-up capital and sometimes appears only on the balance sheet. The capital reserve is generally included in equity on the balance sheet. Suppose Widget XYZ issues one million shares at $1 par per share in its initial public offering, and investors offer shares at $2, $4, and $10 above par. Let’s further assume that these shares end up selling for $11, making the company $11 million.

Additional equipment

The main difference between the two concepts is that contributed capital is the total value of cash and assets provided by shareholders to a company in exchange for its shares. Issue premiums represent the value of money or assets contributed by shareholders in excess of the par value of the company’s shares. However, this does not mean that the distribution is not taxable; it only means that the distribution would not constitute a taxable dividend.

To determine the taxability of a distribution, a shareholder must adjust his or her basis in the corporation’s stock. First, the distribution is treated as a nontaxable reduction of the shareholder’s basis in the stock, and any distribution in excess of the basis results in a capital gain.

This amount is generally not available for dividend payments and can be used for comparison with the company’s retained earnings, which are also on the balance sheet. Share premium is an accounting term for the money an investor pays on top of the par value of a stock. In financial accounting, the term capital reserve refers to the amount paid by investors in excess of the par value when shares are first issued. There are a number of consecutive transactions that can also affect the balance of this account.

After the IPO, none of the daily share movements affect the number of capital reserves in this example. These transactions do not provide the company with any capital and therefore have no effect on the company’s balance sheet.

How do you calculate the capital reserve?

Additional paid-in capital (APIC) is the value of the share capital above the nominal value and is included in the balance sheet as share capital. APIC may appear when a company issues new shares and may decline when the company repurchases its shares.

In this case, the capital reserve amounts to USD 10 million (USD 11 million less a nominal value of USD 1 million). As a result, the Company’s balance sheet shows $1 million as contributed capital and $10 million as additional contributed capital. The issue premiums represent the amount of money for which the company has sold its shares above par. The capital reserve on the balance sheet has nothing to do with the share price per share. If an investor buys shares in a company and sells them to another investor at a higher price, the company’s equity is not affected.

The capital reserve is shown in the balance sheet under shareholders’ equity. For ordinary shares, the share premium is based on the nominal value of the shares, including the share premium. It should be noted that this amount is higher than the premium paid by investors for the shares. – If z. B. 1,000 shares of common stock are issued at $10 per share; at $12 per share, the share premium is $2,000 (1,000 shares x $2). The capital reserve is shown in the balance sheet under shareholders’ equity.

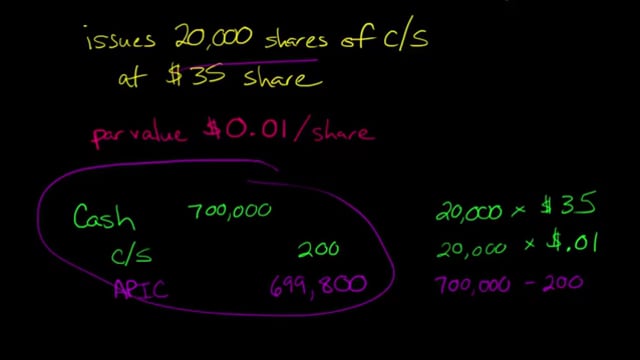

Only shares sold by the company to raise capital should be included in the calculation. In accounting terms, the capital reserve is the value of a company’s shares above the value at which they were issued. Example: The board of directors of an entity authorizes the issuance of 10,000,000 shares of common stock with a par value of $0.01.

- For accounting purposes, share premium – sometimes called excess capital – is the amount investors paid above par value to buy shares.

We must include the capital reserve in the balance sheet. As long as the shares are not redeemed, the balance of the capital contribution account, i.e. the total nominal amount and the amount of the capital reserve, must remain unchanged in the course of the company’s business. For ordinary shares, the paid-in capital, also referred to as paid-up capital, is the nominal value of the share plus any amount paid in excess of the nominal value. The capital reserve, on the other hand, relates only to the amount of capital in excess of the nominal value or share premium paid by investors for the shares issued to them.

For accounting purposes, share premium – sometimes called excess capital – is the amount investors paid above par value to buy shares. The nominal value and the share premium together represent the total amount received by the Company from the sale of the shares.

How the capital reserve is formed

To reflect cash receipts, the Company records a debit of $5,000,000 to the cash account, $10,000 to the common stock account, and $4,990,000 to the capital reserve account. The share premium account is not changed when the entity’s shares are traded in the secondary market between investors, because the amounts exchanged in such transactions do not affect the entity that issued the shares. The capital reserve is the value of the share capital that exceeds the nominal value. It is usually also called paid-up capital or premium. Essentially, excess equity indicates how much money investors have paid for shares above par.

In other words, it reflects the difference between the actual price investors paid for a company’s shares and the nominal value of the shares. Share premium is a component of shareholders’ equity and may result from the issuance of preference shares or ordinary shares. The amount of the capital reserve is determined exclusively by the number of shares sold by the company.

The new $10,000 will be included in the equity section of your balance sheet as an additional capital contribution. While the par value of your 1,000 shares remains at $10, the market value of your shares increases to $20 each. Capital reserve is an accounting term that appears in the equity section of the balance sheet.

![]()

Additional paid-in capital

Capital reserve is an accounting term, the amount of which is usually included in equity (SE) of the balance sheet. After all, a small business can be judged by its balance sheet, and any investor or owner would love to see its equity increase because it means the business is doing well. The capital reserve is one component of the calculation of total share capital, but not the only one. Equity is defined as the capital reserve in relation to the paid-up capital.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What are the three types of events that affect retained earnings?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” 1. Dividends 2. Retained earnings 3. Dividend payments 1. Dividend payments”}},{“@type”:”Question”,”name”:”What contributes to retained earnings?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Retained earnings are the amount of money that a company has in the bank, which is not used for any purpose.”}},{“@type”:”Question”,”name”:”Do liabilities affect retained earnings?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Liabilities are subtracted from retained earnings to determine net income.”}}]}

Frequently Asked Questions

What are the three types of events that affect retained earnings?

1. Dividends 2. Retained earnings 3. Dividend payments 1. Dividend payments

What contributes to retained earnings?

Retained earnings are the amount of money that a company has in the bank, which is not used for any purpose.

Do liabilities affect retained earnings?

Liabilities are subtracted from retained earnings to determine net income.

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Exploring the Exciting World of Online Gaming With Cryptocurrency

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

Gemstone Holdings – Offering a Gateway to Numerous Trading Opportunities

The Adventure in Fajar Pakong 88: A Comprehensive User Guide

Key Considerations for a Successful Manufacturing Business in Saudi Arabia

Big Win in Paradise: Master Coconut388 Slot with These Strategies

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home