Basel III

The Basel III agreement to strengthen the global regulatory framework for banking regulation came into force on 1 January 2014. And the G20 has agreed that the Basel III minimum capital requirements will apply to all systemically important banks. The Basel III regulation aims to improve the quality of bank regulatory capital.

Basel III is a system that the Bank of International Settlements (BIS, formerly known as the Bank for International Settlements) created in 2002 to harmonize international regulatory capital requirements. Basel III was developed in the context of the 1998 Basel II accord, which had been successful in harmonizing capital requirements for banks and other financial institutions.

Basel III is a new European Union regulation that dictates the financial sector’s capital requirements. It’s a key pillar of European Union economic and financial policy, and significantly affects the structure of the financial services industry in Europe.

19. August 2020

Accounting Adam Hill

The term leverage is also used to describe a company’s total debt by comparing debt to assets or debt to equity. A highly indebted company has a debt-to-equity ratio close to or greater than 1.

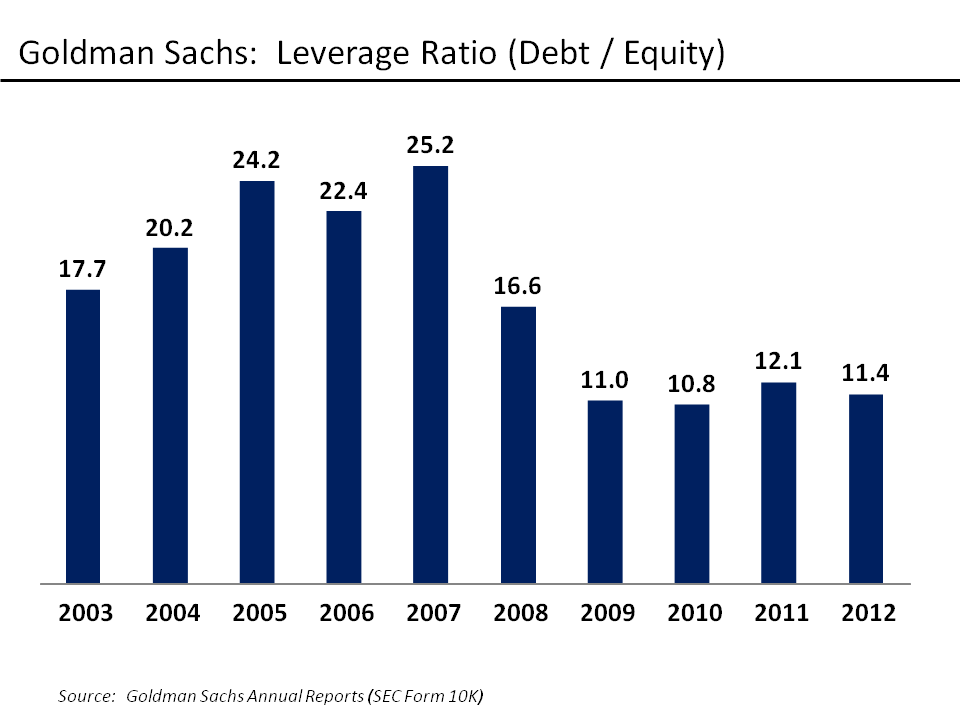

A higher leverage ratio is generally considered safer for a bank because it shows that the bank has more capital relative to its assets (mainly loans). This is particularly useful when the economy is in recession and loans are not being repaid.

In other words: It becomes more difficult to meet financial obligations when the assets of a highly indebted company suddenly become worth less. The leverage ratio (LDF) is a debt ratio that measures the sensitivity of a company’s earnings per share to fluctuations in operating income due to changes in its capital structure.

FedEx has a D/E ratio of 1.78, so there is reason to be concerned about UPS. However, most analysts believe UPS is making enough money to cover its debts. The FDIC and the Comptroller of the Currency impose various forms of capital and reserve requirements on U.S. banks that indirectly affect leverage ratios. After the great recession of 2007-2009, when too-big-to-fail banks became the rallying cry for improving bank solvency, the scrutiny of leverage ratios increased.

Debt to equity ratio

Thus, it is essentially a coefficient that measures the financial condition of a bank. While it is common to have modest amounts of debt, companies with large amounts of debt are exposed to serious risks. High debt repayments eat into revenues and in the most serious cases the company risks bankruptcy. Active investors use a number of different leverage ratios to get an idea of the sustainability of a company’s leverage practices. Each of these basic calculations in isolation provides a somewhat limited picture of a company’s financial strength.

The denominator of the leverage ratio is the Bank’s total exposure, which includes consolidated assets, derivative exposure and certain off-balance sheet exposures. Basel III requires banks to consider off-balance sheet exposures such as commitments to third parties in respect of loans, stand-by letters of credit, acceptances and commercial letters of credit. The main cause of the great financial crisis was the accumulation of excessive debt inside and outside the balance sheet in the banking system. In many cases, banks have built up excessive leverage while maintaining seemingly high risk capital ratios.

Banks have relatively fewer creditors than debtors, making it difficult to repay loans. Therefore, it is worthwhile to have a high level of equity during these periods. For example, suppose a financial institution has $200 billion in total Tier 1 assets. To calculate the capital ratio, they divided $200 billion by $1.2 trillion of risk, resulting in a capital ratio of 16.66%, well above the Basel III requirements. Under Basel III, the minimum Tier 1 capital ratio is 10.5%. It is calculated by dividing a bank’s Tier 1 capital by its total risk-weighted assets (RWA). RWA measures a bank’s credit risk in the context of lending.

The debt-to-equity ratio is the ratio of debt to equity for a company, bank, house, etc. A high debt-to-equity ratio indicates that a company, bank, home or other institution is highly indebted.The Basel III regulations, which will be adopted in late 2011, are designed to make global banking stronger and more resilient during a period of considerable uncertainty.. Read more about basel iii capital requirements and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is Basel III in simple terms?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Basel III is a set of international banking regulations that were introduced in 2010.”}},{“@type”:”Question”,”name”:”What are the 3 pillars of Basel 3?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The 3 pillars of Basel 3 are: 1. A standardized approach to calculating risk-weighted assets for banks and other financial institutions, which is based on the bank’s own internal models. 2. A standardized approach to calculating capital requirements for banks and other financial institutions, which is based on the bank’s own internal models. 3. A standardized approach to calculating liquidity requirements for banks and other financial institutions, which is based on the bank’s own internal models.”}},{“@type”:”Question”,”name”:”How does Basel III work?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The Basel III framework is a set of international banking standards that are designed to strengthen the global financial system. The Basel Committee on Banking Supervision, which is an international body of regulators and bank supervisors, developed the framework. The Basel III framework includes three main pillars: capital requirements, liquidity requirements, and risk-based supervision. Capital requirements are the amount of money banks must have on hand to cover potential losses. The Basel III framework sets a minimum capital requirement for banks, which is 8% of risk-weighted assets. Liquidity requirements are the amount of cash that banks must keep on hand in order to meet their obligations and avoid running out of money. The Basel III framework sets a minimum liquidity requirement for banks, which is 3% of risk-weighted assets. Risk-based supervision is the process of evaluating a bank’s risk profile and determining how much capital it needs to hold. The Basel III framework sets a minimum risk-based capital requirement for banks, which is 8% of risk-weighted assets. What are the benefits of Basel III? The benefits of Basel III include: Strengthening the global financial system Providing a framework for international banking standards Ensuring that banks have enough capital to cover potential losses Ensuring that banks have enough liquidity to meet their obligations and avoid running out of money What are the drawbacks of Basel III? The drawbacks of Basel III include:”}}]}

Frequently Asked Questions

What is Basel III in simple terms?

Basel III is a set of international banking regulations that were introduced in 2010.

What are the 3 pillars of Basel 3?

The 3 pillars of Basel 3 are: 1. A standardized approach to calculating risk-weighted assets for banks and other financial institutions, which is based on the bank’s own internal models. 2. A standardized approach to calculating capital requirements for banks and other financial institutions, which is based on the bank’s own internal models. 3. A standardized approach to calculating liquidity requirements for banks and other financial institutions, which is based on the bank’s own internal models.

How does Basel III work?

The Basel III framework is a set of international banking standards that are designed to strengthen the global financial system. The Basel Committee on Banking Supervision, which is an international body of regulators and bank supervisors, developed the framework. The Basel III framework includes three main pillars: capital requirements, liquidity requirements, and risk-based supervision. Capital requirements are the amount of money banks must have on hand to cover potential losses. The Basel III framework sets a minimum capital requirement for banks, which is 8% of risk-weighted assets. Liquidity requirements are the amount of cash that banks must keep on hand in order to meet their obligations and avoid running out of money. The Basel III framework sets a minimum liquidity requirement for banks, which is 3% of risk-weighted assets. Risk-based supervision is the process of evaluating a bank’s risk profile and determining how much capital it needs to hold. The Basel III framework sets a minimum risk-based capital requirement for banks, which is 8% of risk-weighted assets. What are the benefits of Basel III? The benefits of Basel III include: Strengthening the global financial system Providing a framework for international banking standards Ensuring that banks have enough capital to cover potential losses Ensuring that banks have enough liquidity to meet their obligations and avoid running out of money What are the drawbacks of Basel III? The drawbacks of Basel III include:

Unlock Your Coolest Summer Yet: Dive Into Quality Self-Care Trends

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Gemstone Holdings – Offering a Gateway to Numerous Trading Opportunities

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

The Adventure in Fajar Pakong 88: A Comprehensive User Guide

Role, Earnings and Spending of Gil in Final Fantasy 14

Essential Skills for Writing a Literature-Based Dissertation – A Complete Guide

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home