Accumulated depreciation

Accumulated Depreciation is a cost allocation method that accounts for the wear and tear on plant and equipment from the time it is purchased to the time it is to be replaced. It’s a common method of accounting in all industries. This blog post will compare the common costs of purchasing a used vehicle as a new vehicle. We will compare the cost of a new vehicle to the cost of a used vehicle at the time of purchase. It will show that the only real difference between a new and used vehicle is the time that has passed since the purchase.

Accumulated depreciation is a concept that is often overlooked when calculating the value of an asset or the cost of a business acquisition. Accumulated depreciation represents the total amount of depreciation that has been taken or applied to a company’s assets over a specific time period. Over time, this can represent a significant amount of money that has been wasted due to missed opportunity.

Since the year began, I’ve been keeping track of my business expenses in a spreadsheet in Google Sheets. For the most part, this spreadsheet has been used to track how much cash I have in the bank each month. However, I’ve also been keeping track of some other items, such as business insurance (which I take out monthly), auto insurance (which I take out semi-annually), ad hoc expenses (such as (gas station) stubs I receive and expense to keep track of business travel), and accumulating depreciation on my office furniture, which I have been tracking for a few years now.. Read more about accumulated depreciation formula and let us know what you think. Household Accumulated depreciation

3.7.2020

Adam Hill Accounts

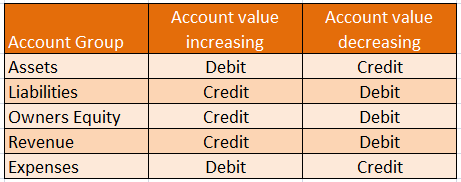

Why Accumulated Depreciation is a Credit

Is depreciation an asset or a liability?

The main journal entry for depreciation is a debit to the depreciation expense account (which appears in the income statement) and a credit to the accumulated depreciation account (which appears as a settlement account in the balance sheet and reduces the amount of fixed assets).

Depreciation systematically transfers the value of the asset from the balance sheet to the income statement over its useful life. A simplified version of these adjustments is to recognize a special deferred tax asset in the balance sheet, which is used to adjust the difference between the income statement and the cash flow statement. This deferred tax asset decreases over time until GAAP income and IRS income match at the end of the straight-line depreciation schedule.

However, accumulated depreciation plays an important role in reflecting the value of the asset on the balance sheet. The purpose of depreciation is to allocate the cost of a productive asset with a useful life of more than one year to the income generated by its use. The cost of the asset is generally allocated over the years in which the asset is used.

Defining a journal entry for depreciation

Each year the depreciation account is debited by writing off a portion of the asset for that year, and the accumulated depreciation account is credited with the same amount. Accumulated depreciation increases over time as depreciation expense is allocated to the cost of an asset.

The usual method for calculating depreciation expense is the straight-line method. Depreciation is an accounting method that spreads the cost of a tangible asset over time. Companies should ensure that they choose an appropriate depreciation method that accurately reflects the cost of the asset and the recognition of the cost. Depreciation and impairment losses are recognized in the income statement, the balance sheet and the cash flow statement. It can therefore have a major impact on the financial performance of the whole company.

The displays have a useful life of 10 years and have no residual value. Applying the straight-line method, depreciation would be $1,000 per month ($120,000 divided by 120 months). The monthly entry to record depreciation is a debit entry of $1,000 to the depreciation expense account on the income statement and a credit entry of $1,000 to the accumulated depreciation account on the balance sheet. Accumulated depreciation is the accumulated depreciation of an asset that has been recorded. Tangible fixed assets, such as B. Land and buildings are fixed assets.

Depreciation is charged in the year of acquisition and annually over the remaining useful life of the asset. Accumulated depreciation allows investors and analysts to see how much of the value of an asset has been depreciated.

It is taken into account when companies record the depreciation of their fixed assets through depreciation. Tangible assets such as machinery, equipment or vehicles deteriorate over time and gradually lose their value. Unlike other expenses, depreciation is reported in the income statement as a non-cash expense, indicating that no cash was transferred when the expense was incurred. Suppose a retailer buys displays for his store in the amount of $120,000.

Impairment is a method of recording changes in the value of an asset. Depreciation also affects corporate tax and is reflected in your tax return.

- Depreciation is defined as the cost of the asset involved in generating income over its useful life.

- Depreciation charges affect the value of enterprises and units because the accumulated depreciation recorded for each asset reduces its carrying value in the balance sheet.

Why is cumulative depreciation a credit?

The most fundamental difference between depreciation and accumulated depreciation is that one is recorded as an expense in the income statement and the other as an offsetting item in the balance sheet. The journal entry for depreciation is used to apply the correspondence principle. Each accounting period, a portion of the cost of certain assets (equipment, building, vehicle, etc.) is transferred from the balance sheet to the depreciation account. The objective is to match the cost of the asset with the revenue of the accounting periods in which the asset is used.

Depreciation is an additional charge on the cost of an asset over its estimated useful life. The use of the depreciation method allows an entity to depreciate over time the cost of an asset while reducing its carrying amount. Initially, most fixed assets are purchased on credit, which also allows them to be repaid over time. Thus, the initial entries for the first payment of assets are a credit to the accounts payable account and a debit to the fixed assets account.

Example of calculating depreciation expense on a straight-line basis – Suppose a truck is purchased with a value of $10,000, a residual value of $5,000, and a useful life of 5 years. The depreciation amount for the first year is $1,000 (10,000 – 5,000 / 5). The journal entry for this transaction is a debit to depreciation of $1,000 and a credit to accumulated depreciation of $1,000. On the balance sheet, the entity uses cash to pay for the asset, which initially results in a transfer of the asset.

After three years, the book value is $200. Depreciation expense is recorded using the straight-line method and management will retire the asset. Any gain or loss above or below the estimated residual value is recognised and the carrying amount under property, plant and equipment in the balance sheet ceases to exist. For example, if a business purchases a car for $30,000 and plans to use it for the next five years, the depreciation expense will be spread over five years at $6,000 per year. Each year the depreciation account is debited with $6,000 and the capital asset account is credited with $6,000.

Depreciation entries are a debit for depreciation expense and a credit for accumulated depreciation of assets. Any recognition of depreciation expense increases the balance of depreciation expense and decreases the cost of the asset. Accumulated depreciation is charged to capitalized assets.

Is depreciation a liability? Why or why not?

After five years, the cost of the car is completely used up and the book value is zero. Depreciation allows companies to avoid having to deduct a large part of the cost from the profit and loss account in the year of purchase of an asset. Depreciation spreads the cost of an asset over the years of its estimated useful life.

Since the underlying asset does not retain its value over time (like cash), its carrying value is expected to decline gradually. Depreciation costs gradually reduce the cost of tangible fixed assets, so that the value of the assets is correctly reflected in the balance sheet.

When depreciation expense appears in the income statement, instead of reducing cash in the balance sheet, it is added to the accumulated depreciation account. Over time, the accumulated depreciation balance is increased by the depreciation until it reaches the original cost of the asset. Stop depreciating at this point, as the value of the assets is now reduced to zero. The depreciation method selected shall be consistent with the nature of the asset, its intended use in the entity, its estimated useful life and its residual value. This amount reduces both the cost of the asset and the income for the period.

Become a PRO or PRO Plus member and get lifetime access to our premium content

Depreciation is defined as the cost of the asset involved in generating income over its useful life. In accounting terms, depreciation is the allocation of the cost of acquiring and producing assets to the periods in which the assets are used (depreciation based on the principle of equality of costs and revenues). Depreciation charges affect the value of enterprises and units because the accumulated depreciation recorded for each asset reduces its carrying value in the balance sheet. Generally, costs are allocated as depreciation expense over the periods in which the asset is expected to be used. These expenses are recorded by the entities for financial and tax reporting purposes.The idea of depreciation is quite simple. Instead of buying a new car which is depreciated over several years, you can buy a car that’s been depreciated.. Read more about what is accumulated depreciation classified as and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is accumulated depreciation on balance sheet?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accumulated depreciation is the total amount of depreciation that has been recorded on a company’s balance sheet.”}},{“@type”:”Question”,”name”:”How accumulated depreciation is calculated?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accumulated depreciation is calculated by multiplying the cost of an asset by its useful life.”}},{“@type”:”Question”,”name”:”What is accumulated depreciation and example?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accumulated depreciation is the total amount of depreciation that has been taken on an asset. It is calculated by adding the cost of the asset to its accumulated depreciation.”}}]}

Frequently Asked Questions

What is accumulated depreciation on balance sheet?

Accumulated depreciation is the total amount of depreciation that has been recorded on a company’s balance sheet.

How accumulated depreciation is calculated?

Accumulated depreciation is calculated by multiplying the cost of an asset by its useful life.

What is accumulated depreciation and example?

Accumulated depreciation is the total amount of depreciation that has been taken on an asset. It is calculated by adding the cost of the asset to its accumulated depreciation.

Unlock Your Coolest Summer Yet: Dive Into Quality Self-Care Trends

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Gemstone Holdings – Offering a Gateway to Numerous Trading Opportunities

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

The Adventure in Fajar Pakong 88: A Comprehensive User Guide

Role, Earnings and Spending of Gil in Final Fantasy 14

Essential Skills for Writing a Literature-Based Dissertation – A Complete Guide

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home