Accrued Income

Accrued income is the income that is accrued in the system when you are busy working or earning money. It is different from income which you may expect to gain from your job. Accrued income is not the same as interest, the income earned from the money that is earn in your bank account.

Income is the amount of money that a company earns. Accrued income is the income that a company has earned, but not yet paid out to its owners. A company’s cost of goods sold is also its accrued income. The company accrues income in two ways: 1) when it pays its bills, and 2) when it incurs expenses.

Many of us have heard about Accrued Income at some point: it’s the additional amount of money you make as you travel down the path of success. However, what it comes down to is that it’s the sum total of the additional income you’ve earned as a result of actions you’ve taken. It’s a measure of how much work you’ve put into your business and the results it’s brought you.. Read more about accrued income example and let us know what you think. Accounts Home Accruals

15. May 2020

Accounting Adam Hill

The debit entry for wages and salaries payable offsets the credit entry for cash payments or items payable. An entity that adopts the accrual basis of accounting recognises revenue and expenses in the period in which they are incurred regardless of when the payment is made. This differs from the cash basis method, in which an entity recognises revenues and expenses only when cash is received or paid. The two concepts or principles used in accrual accounting are the revenue recognition principle and the conformity principle.

Although the accrual accounting method is time consuming as many journals have to be kept. This method allows for a more accurate assessment of the company’s transactions and events for each period. This fuller picture helps users of the financial statements better understand the company’s current financial position and predict its future financial position. When the company’s accounting department receives an invoice for the total amount of wages due, the vendor account is credited. Trade payables are included in current liabilities on the balance sheet and represent the Company’s current liabilities.

No provision can be made for depreciation and doubtful debts. Reversal reserves can therefore not be used to reverse write-offs or bad debts.

Deferred charges are charges that have been incurred but for which there is no proof of expenditure yet available. Instead of documenting the expense, a journal entry is created to record the accrual and the offsetting liability (which is typically recorded as a current liability on the balance sheet).

After the new year’s payment, the liability account is reduced by a debit and the cash account is reduced by a credit. In a double-entry bookkeeping system, the accrual account is the adjustment for accruals, which appears in the balance sheet. The counterpart of sales revenue is the prepaid expenses account, which is also included in the balance sheet. Therefore, an accrual accounting entry for accrued expenses affects both the balance sheet and the income statement. Under generally accepted accounting principles (GAAP), accrual accounting is preferred.

An adjustment entry affects at least one balance sheet account and one income statement. In the case of payroll, the accounts concerned can be the imputed payroll (balance sheet) and payroll (profit and loss account). At the end of the reporting period, the entity makes adjustments to recognise costs incurred but not yet paid. Note that we are talking about companies that use accrual accounting.

If the original entry is reversed (showing that you paid the expense), it is removed from the balance sheet. An example of deferred spending is employee bonuses earned in 2019 but not paid out until 2020. The 2019 financial statements should reflect the premium cost that employees will earn in 2019 and the premium liability that the company expects to pay. Therefore, prior to the release of the 2019 financial statements, this accrual will be recorded in the adjustment journal as a debit to the expenditure account and a credit to the liability account.

The recording of accrued income is normally a credit to the income statement and a debit to the accrued income account. Do not allow deferred revenue to be reflected in the Accounts Receivable account, as this account is for accounts receivable, which are normally posted to the account by the accounting software’s billing module. For example, an entity that holds bonds will include interest expense in its monthly financial reports even though interest on bonds is normally paid semiannually. The interest expense included in the adjustment entry is the amount accrued at the balance sheet date. The corresponding interest liability is recognised in the balance sheet.

Without a journal entry, the expense would not have appeared at all in the entity’s financial statements in the period in which it was incurred, resulting in a surplus of profit for that period. In short, accruals are recorded to improve the accuracy of financial reporting so that expenditure better matches the revenue to which it relates.

- Deferred revenue is revenue that is earned or costs that are incurred that affect the entity’s net profit in the income statement even though the cash flows associated with the transaction have not yet changed hands.

- Accrued expenses include trade payables, trade receivables, taxes payable and accrued interest received or payable.

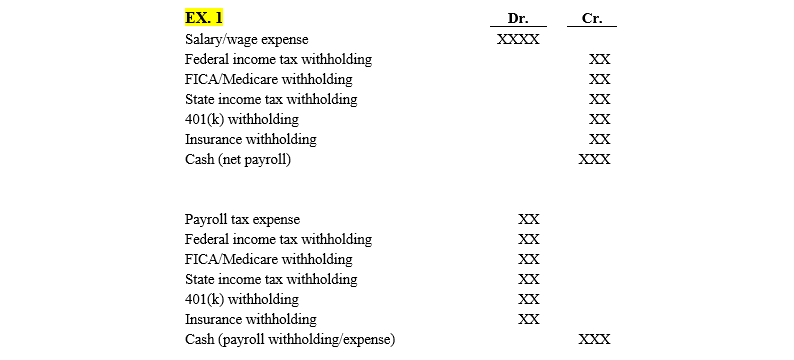

Imputed payroll costs are recorded as a debit entry to record employee payroll costs, being the amount of total earnings accrued by employees for work performed at the end of the pay period. Deferred wages and salaries are recognised as an operating expense in the income statement in the period in which they are incurred, regardless of whether the entity has made cash payments for the wages and salaries payable.

The dissolution provisions are optional and can be applied at any time as they have no effect on the financial statements. Accruals can be used to adjust revenues, expenses, and deferred income to match the current accounting period.

Accounting tools

The concept of accrual accounting is also used in generally accepted accounting principles (GAAP) and plays a key role in accrual accounting. Under this accounting method, revenues and expenses are recognized at the time of the transaction regardless of whether cash is received or disbursed. In this way, the entity may assess its financial position by considering the amount of cash it expects to receive, rather than the amount of cash it has currently received.

How to calculate salary benefits

The credit side reduces the balance in the cash account. When companies withhold taxes from employee wages, cash payments are reduced by the amount of taxes to arrive at the employees’ take-home pay. Companies then use another payroll tax credit to make up the difference between total wages and net wages.

The credit in the accounts payable account increases the company’s creditors. Thus, the greater the time lag between the time wages are earned and the time they are actually paid, the greater the wage costs of the firms are financed by their employees. Accruals are normally recorded by making corrective journal entries at the end of the period.

Companies operating on a cash basis do not use accruals and the corresponding standard entries. Deferred revenue is recorded when you have received a sale from a customer but have not yet invoiced him (once the customer is invoiced, the sale is recorded in the accounting program through the invoicing module). Deferral of payment of income may extend over several billing periods until the time is right to bill the customer. However, prepaid expenses and accrued expenses should be classified as current assets and are therefore included in current assets in the balance sheet.

Comparisons between log entries

The use of accrual accounting significantly improves the quality of the information contained in the financial statements. Before the use of accrual accounting, accountants only recorded cash transactions. Unfortunately, cash transactions do not provide insight into other important activities, such as. B. Income resulting from loans to customers or future obligations of the company. By recording accruals, a company can estimate the amount it will owe in the near term and the cash it expects to receive. It also allows an entity to recognise assets that have no monetary value, such as. B. Goodwill.

In accrual accounting, the Accounting Officer corrects revenue received but not yet recorded in the general ledger and expenditure incurred but also not yet recorded. At the end of each reporting period, adjustments are made by means of journal entries to reflect these amounts in the financial statements. When a provision is made for an expense, the expense account must be debited and the provision account (which is on the balance sheet) credited. When you incur an expense, it will therefore appear on the liabilities side of the balance sheet.

Is payroll an accrual expense?

The term accumulation simply means accumulation. Payroll refers to wages, salaries, commissions, bonuses and allowances earned and payable by employees. It’s simple: Liabilities arising from employee payroll costs already incurred but not yet paid are referred to as salaries to be paid.

Try our payroll software with an optional free 30-day trial!

Deferred revenue is revenue that is earned or costs that are incurred that affect the entity’s net profit in the income statement even though the cash flows associated with the transaction have not yet changed hands. Provisions also affect the balance sheet, as they include non-monetary assets and liabilities. Accrued expenses include trade payables, trade receivables, taxes payable and accrued interest received or payable. Since the company has actually incurred personnel expenses for 12 months, an adjustment entry is made at the end of the pay period for the expenses of the last month. The adjustment will be made as of December 31 and will debit the personnel expense account in the income statement and credit the personnel liability account in the balance sheet.Income is the main way that the majority of people pay for their living expenses. It is the main source of wealth for most people. Income is also a vital component of an individual’s quality of life and quality of life is a key component of happiness and well-being.. Read more about accrued income and expenses and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is meant by accrued income?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accrued income is the amount of money that has been earned but not yet received.”}},{“@type”:”Question”,”name”:”What is accrued income with example?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accrued income is the amount of money that you have earned but not yet received.”}},{“@type”:”Question”,”name”:”What is accrued income in balance sheet?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accrued income is the amount of money that has been earned but not yet received.”}}]}

Frequently Asked Questions

What is meant by accrued income?

Accrued income is the amount of money that has been earned but not yet received.

What is accrued income with example?

Accrued income is the amount of money that you have earned but not yet received.

What is accrued income in balance sheet?

Accrued income is the amount of money that has been earned but not yet received.

Unlock Your Coolest Summer Yet: Dive Into Quality Self-Care Trends

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Gemstone Holdings – Offering a Gateway to Numerous Trading Opportunities

Winning Secrets, Features, and Immersive Gaming Experience: Mastering Ibc88play

The Adventure in Fajar Pakong 88: A Comprehensive User Guide

Role, Earnings and Spending of Gil in Final Fantasy 14

Essential Skills for Writing a Literature-Based Dissertation – A Complete Guide

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home