A Beginner’s Guide to The Accounting Cycle

For many people the thought of learning about accounting is daunting, especially those who have never had to pay close attention to records and report. But accounting is something that we all experience in one way or another and that sooner or later we will have to deal with, whether it’s paying the bills, filing your taxes, or some other form of financial record keeping.

The Accounting Cycle is the name given to the way companies use accounting data to make decisions about how much money to invest in their business. The cycle starts with collecting accounting data, and then analyzes it, and moves on to (hopefully) investing the resulting information in their business. In the world of Accounting, the cycle is very much like a machine, and companies show an obsession with improving the machine.

I was first introduced to the accounting cycle while studying information systems at college. As an accounting major, I was required to take a course called “spreadsheet modeling” that taught me how to use a spreadsheet as a way to keep track of sales, expenses and income. This is a simple, but important concept that I wanted to share with my readers. About a month ago, I was looking for a job and came across the job postings for a software company that provides accounting software and services to small businesses. One of the requirements for the position was to have a basic understanding of the accounting cycle.. Read more about beginners meaning and let us know what you think. Accounting Home Beginner’s Guide to the Accounting Cycle

12. May 2020

Accounting Adam Hill

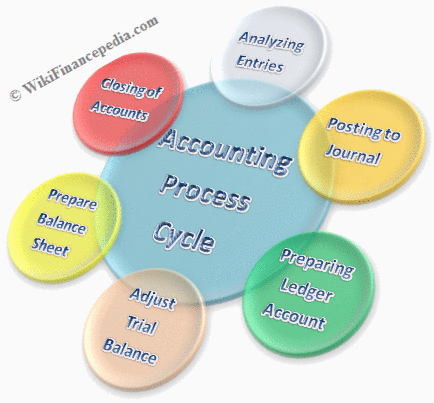

Keeping accurate financial records is not an option. The accounting cycle is the system by which companies record their transactions in order to prepare the necessary financial statements. However, many business owners don’t fully understand this process, which is why we’ll cover it in today’s article. Closing entries are made at the end of the reporting period to transfer these temporary accounts to permanent accounts in the balance sheet or profit and loss account. The accounting cycle is the process of a complete sequence of accounting transactions in the correct order during each accounting period.

Then each transaction is recorded in the journal – a list of financial transactions in chronological order. The journal entries are then recorded in the books with the increases and decreases in specific asset, liability and equity accounts.

If the entries are made without errors, the total balance of all accounts with a positive balance is equal to the total balance of all accounts with a negative balance. After closing, prepare a trial balance to verify that the total debit amount matches the total credit amount in the general ledger.

Using the balance sheet, they regularly record financial transactions that provide insight into the financial health of the business over time and predict its longevity. After preparing the journal and recording all corrections, many companies still prepare a trial balance based on their general ledger and accounts.

These balances are carried forward to the following year as opening balances. The accounting cycle refers to the process of financial reporting. It starts with the analysis of commercial transactions, their recording in journals and their entry in ledgers.

It shows the balances of all accounts, including adjusted accounts, at the end of the reporting period. Thus, the final result of this adjusted trial balance shows the impact of all financial events that occurred during the reporting period. This is the transfer of information from the journal to the general ledger. The entries are required to have a complete record of all accounting transactions in the general ledger, which is used to prepare the company’s financial statements.

BlackLine Accounting Process Automation increases the speed, accuracy and reliability of the reconciliation and adjustment process by automating routine and extensive transaction processes. Based on a system of debits and credits known as double entry bookkeeping, accountants use the general ledger to track the flow of money in and out of the business.

Computers have simplified many of these tedious tasks, and sites like Sleek AU offer all-inclusive accounting services for all your business paperwork. The accounting cycle refers to the process of financial reporting, from the business transaction to the preparation of the report. The first step in this cycle is to analyze the data collected from many sources.

Set up an adjusted trial balance to verify that the total amount of debits matches the total amount of credits in the general ledger. Adjustment entries are journal entries made at the end of an accounting period that change the ending balance of various general ledger accounts. These adjustments are made to better align the reported results with the actual financial position of the company. The restatements are consistent with the principles of yield recognition and alignment. The consolidated statement of temporary income is then closed on the drawing up of the financial statements.

Unadjusted statement of comprehensive income

All transactions that have a financial impact on the business – sales, payments to employees and suppliers, interest and tax payments, inventory purchases and others – must be documented. The accountant must check that the documents are complete. Using generally accepted accounting principles, auditors record and present the financial data of all companies in the same way. They report their findings in the annual financial statements, which summarize the company’s business transactions over a period of time.

Booking cycle: 9-step booking process

- This is a continuous process throughout the reporting period.2Journal entriesBased on the above documents, enter journal entries according to the double-entry bookkeeping system where debit and credit balances remain the same.

- 1Collection and analysis of accounting documentsThis is a very important step where you study and analyze the source documents.

The general ledger totals for each account are summarized in a trial balance, which is used to confirm the accuracy of the figures. These values are used in the preparation of the annual financial statements and management reports. After all, people analyze these reports and make decisions based on the information they contain. Designed to complement existing financial systems, BlackLine fills the gaps in ERP and CPM systems to help businesses improve operational efficiency, real-time visibility, control and compliance. This automates financial close and end-to-end accounting and facilitates decision making across the enterprise.

The accounting process is a sequence of operations that begins when a transaction occurs and ends when it is recognized in the financial statements at the end of the reporting period. DetailsObjectiveCash $11,670Accounts receivable-0Pre-paid insurance2,420Stocks3,620Furniture16,020Loans-220Unrealized consulting income-3,000Debt-6,000M. If the sum of the debit entries in the trial balance is not equal to the sum of the credit entries, an error occurred while entering or posting the entries. At the end of the reporting period, the foreground balance is calculated as the fourth step in the accounting cycle. The trial balance shows the company the unadjusted balances on each account.

1Collection and analysis of accounting documentsThis is a very important step where you study and analyze the source documents. For example, cash, bank, sales and purchase administration. This is a continuous process throughout the reporting period.2Journal entriesBased on the above documents, enter journal entries according to the double-entry bookkeeping system where debit and credit balances remain the same. This process is repeated throughout the booking period.3 Bookings in the accountsThe debit and credit balances of all the above accounts affected by the bookings are recorded in the accounts.

We use a trial balance to record all information in the financial statements. As a result of these entries, the balances of all income and expense accounts are reduced to ZERO.

Balance after clearance of accounts

As mentioned above, the three main financial statements are the balance sheet, the income statement and the cash flow statement. In a double-entry bookkeeping system, pairs of related financial transactions in asset, liability, income, expense or capital accounts are recorded at each entry. By debiting an amount from one account and crediting an equal amount to another account, the total debit amount is equal to the total credit amount of all accounts in the general ledger.

Point-of-sale technology can help combine steps 1 and 2, but companies also need to track their costs. The choice between accrual and cash accounting determines when transactions are formally recorded. Remember that accrual accounting requires a reconciliation between income and expenses, and both must be recorded at the time of sale.

Identification and analysis of trade transactions

The totals of the general ledger are then added together in a trial balance, which confirms the accuracy of the figures. The auditor then prepares the financial statements and reports. The final step is to analyze these reports and make decisions.

When the debit is equal to the credit, the balance sheet equation is in balance. When the accounting equation is balanced, the financial statements are connected. The accrual basis of accounting requires an entity to prepare its financial statements on a periodic basis. Therefore, the booking run is performed once in each booking period. The accounting cycle begins with the recording of individual transactions and ends with the preparation of financial statements and closing entries.

The uncorrected trial balance then goes to step five for review and analysis. The second step in this cycle is to create journal entries for each transaction.

*10. Reverse inputs: Optional step at the start of a new reporting period

Since we use a dual accounting system, the sum of all debit and credit balances as shown in the trial balance remains the same. Since in most cases we have used accrual accounting to determine the correct value of the revenue, expense, asset and liability accounts, we must make these correction entries. This is done at the end of each accounting period.6 Adjusted Trial Balance Using the above correction entries, we create an adjusted trial balance.I wish there was a way to teach accounting to people who aren’t accountants. For some reason, the learning curve for accounting is so steep that most people can’t understand it, even when they’re interested in the subject. So, I decided to write a beginners guide to accounting that I hope will help people to understand it.. Read more about just a beginner and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”Is it okay to be a beginner?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Yes, it is okay to be a beginner.”}},{“@type”:”Question”,”name”:”Is beginner a proper noun?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” No, beginner is not a proper noun.”}},{“@type”:”Question”,”name”:”How do u spell beginner?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” B-E-D-A-R-I-E-R”}}]}

Frequently Asked Questions

Is it okay to be a beginner?

Yes, it is okay to be a beginner.

Is beginner a proper noun?

No, beginner is not a proper noun.

How do u spell beginner?

B-E-D-A-R-I-E-R

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Can PTSD Be Cured? Exploring Treatment Options and Recovery Paths

The 5 Countries for Offshore Manufacturing

The Versatile World of Sock Sleeves

BetterThisWorld com: Unveiling New Perspectives

BetterThisWorld.com: Revolutionizing Social Impact Online

National Debt Relief: Empowering Women Through Financial Education

Sustainable Investments and Ethical Business Practices for Betterthisworld Money

On the Road and On Task: A Practical Approach to Working While Traveling

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home