Material variance

Material variance is the difference between the value of an asset and the price of that asset. If the price of an asset is $100, and the value of that asset is $100, then the material variance is $100. If the price of an asset is $100, and the value of that asset is $50, then the material variance is $50. The material variance is the difference between what a financial instrument is worth and what it is priced at.

This is the first theme blog for 2014, and we’re starting with the subject that is bubbling up in the stock market lately: “Material variance”. The thesis is that stocks have been on a strong run recently, and there are sound reasons for that. Yet, sometimes the material from the financial media just doesn’t seem to acknowledge that.

Home » Bookkeeping » Material variance

Jul 6, 2020

Bookkeeping by Adam Hill

Diagramming direct materials variances

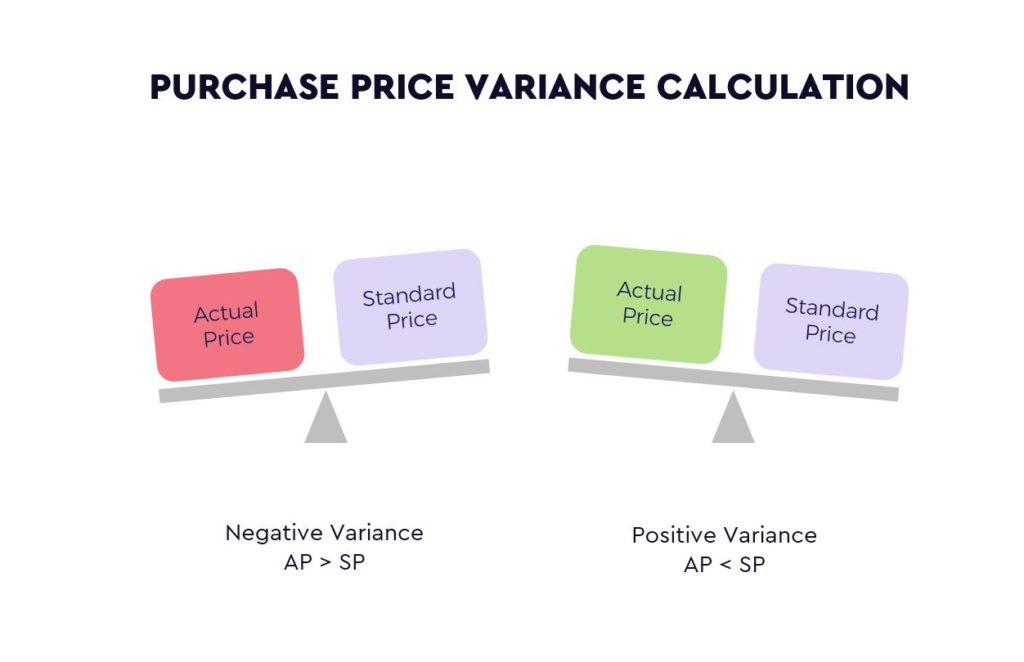

As the cost of goods changes, your amount budgeted may come in a bit high or low. For budgeting purposes, many companies determine a standard cost at the beginning of each year that is used as the estimated price of goods throughout the year. The term “purchase price variance,” or PPV variance, is used to show the difference between the estimated and actual costs in accounting.

To calculate work-in-progress inventory, add the cost of direct materials to direct labor and manufacturing overhead for the incomplete inventory. Accountants typically use standard costing to estimate the value of direct materials, direct labor and manufacturing overhead in work-in-progress inventory. Direct materials cost is the sum of all direct materials costs incurred during the accounting period.

The standard rates calculated for batch and product level activities do not vary with production volume. This is a fundamental difference between ABC and traditional variance analysis. This example illustrates the accounting entries for purchase price variance and exchange rate variance for a standard cost item.

When complete, capitalizable variances should be recorded in a “standard-to-actual” reserve within inventory on the balance sheet with the remainder being appropriately expensed through the income statement. This reserve has the effect of adjusting the company’s inventory balances to “actual,” which is appropriate under GAAP. On a net basis, the purchase price variance is really the difference between standard cost of the material and the actual invoice price of the material. The materials price variance can be computed either when materials are purchased or when they are placed into production.

The actual cost less the actual quantity at standard price equals the direct materials price variance. The difference between the actual quantity at standard price and the standard cost is the direct materials quantity variance. The total of both variances equals the total direct materials variance. In this lesson, we looked at the importance of standard costs for companies. Remember that a standard cost is the amount that you expect to pay for a good or service, especially when it comes to creating something.

How do you find the direct materials price variance?

Purchase price variance. This is the difference between the standard and actual cost per unit of the direct materials purchased, multiplied by the standard number of units expected to be used in the production process. This variance is the responsibility of the purchasing department.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What are the different types of material variances?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Material variances are the differences between the actual and budgeted quantities of material.”}},{“@type”:”Question”,”name”:”How do you calculate total materials variance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The total materials variance is calculated by adding the materials cost variance to the labor cost variance.”}},{“@type”:”Question”,”name”:”Why do we calculate material variance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The material variance is calculated to determine the difference between the actual and budgeted cost of a product.”}}]}

Frequently Asked Questions

What are the different types of material variances?

Material variances are the differences between the actual and budgeted quantities of material.

How do you calculate total materials variance?

The total materials variance is calculated by adding the materials cost variance to the labor cost variance.

Why do we calculate material variance?

The material variance is calculated to determine the difference between the actual and budgeted cost of a product.

A Detailed Guide to Purchasing Wholesale Flowers

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Can PTSD Be Cured? Exploring Treatment Options and Recovery Paths

The 5 Countries for Offshore Manufacturing

BetterThisWorld com: Unveiling New Perspectives

BetterThisWorld.com: Revolutionizing Social Impact Online

Sustainable Investments and Ethical Business Practices for Betterthisworld Money

Betterthisworld Business Social Media Marketing Strategies

Building Your Crypto Knowledge: Must-Read Books and Resources for Enthusiasts

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home