Intercompany eliminations

While there is no specific “business definition” for what an intercompany eliminations (ICD) is, in short, it is a way to remove intercompany transactions from a financial statement. The objective of this article is to provide a short introduction to ICDs and why they are important.

The Board of Directors (BOARD) of Cherrygrind, Inc. (CGI) has approved the following Intercompany Eliminations:

General Accounting Elimination of intra-group transactions

10. August 2020

Accounting Adam Hill

Intercompany accounting is a set of procedures used by a parent company to eliminate transactions between its subsidiaries. If z. B. a subsidiary sells goods to another subsidiary; this is not a valid sale from the perspective of the parent because the transaction was internal. Therefore, the sale should be eliminated from the accounts when preparing the consolidated financial statements of the parent company.

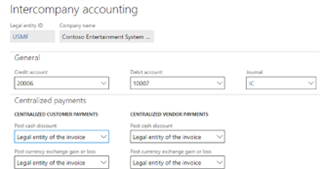

What are journal entries for intercompany accounts?

You can track financial performance and generate reports for an unlimited number of affiliates in your organization. Connected companies can exchange billing dates, calendars and currencies, as well as non-financial data. Accounting for intercompany transactions is an essential process for any company with at least one subsidiary. This removes from the financial books all transactions that have taken place between the departments of the company. This intercompany reconciliation significantly reduces the potential for misrepresentation of the company’s financial statements.

Separate accounts are kept for each individual company, but not for the group. The amounts of the individual subsidiaries are added together to determine the consolidated amounts. Elimination entries are made to eliminate the effect of intercompany transactions. Intra-group accounting is the recording of financial transactions between different legal entities within the same parent company. Because these entities are related, the transactions between them are not independent and the entities cannot recognize gains or losses on those transactions in the consolidated financial statements.

Vision uses these accounts to process intercompany salaries and expenses. Intercompany eliminations refer to the process of eliminating intercompany transactions when preparing consolidated financial statements.

However, this process involves many relationships, and the paperwork for relationships within a company can be quite complicated. Change the journal entry slightly when the customer accepts the cash discount. Enter the total invoice amount as a credit to the customer account, reducing receivables. The actual amount received is recorded on the debit side of the cash account, reflecting the physical payment to the bank.

A summary report of account transfers would make it much easier to prepare a series of income tax adjustments in our general ledger each year, without staff having to track each entry in Oracle. An IC merger occurs when two branches of the parent company come together as a result of a transaction. One subsidiary is the seller and another subsidiary is the buyer. Thus, to ensure that the financial statements reflect the correct figures, they must be reconciled.

What are business-to-business transactions?

Intercompany accounting is a set of procedures used by a parent company to eliminate transactions between its subsidiaries.

The following are some examples of intra-group transactions and their accounting treatment. Intercompany eliminations (ICE) are performed to eliminate gains/losses from intercompany transactions. Receivables, payables, investments, equity, income, cost of sales, gains and losses are not recognized in the consolidated financial statements until they are realised through a transaction with an external party. I was wondering if you, Jake, or some other expert would like to go back. I work in the tax department of a subsidiary of a very large multinational group whose headquarters are in France.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”Which intercompany transactions should be eliminated?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The following transactions should be eliminated: 1. Company A purchases $100,000 of goods from Company B. 2. Company A sells $100,000 of goods to Company B. The following transactions should be eliminated: 1. Company B purchases $100,000 of goods from Company C. 3. Company A sells $100,000 of goods to Company C. Company C purchases $100,000 of goods from Company D. 4. Company A sells $100,000 of goods to Company D. 4. Company D purchases $100,000 of goods from company E. 2. 3. Company C purchases $100,000 of goods from company D. 4″}},{“@type”:”Question”,”name”:”Why must intercompany transactions be eliminated?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The elimination of intercompany transactions is a key component of the proposed tax reform. The elimination of these transactions will reduce the complexity and compliance costs associated with these transactions. What is the proposed tax reform? The proposed tax reform would reduce the corporate income tax rate from 35% to 20%. The proposal also includes a territorial system for taxation, which would eliminate the current worldwide taxation system.”}},{“@type”:”Question”,”name”:”What is an elimination entry in consolidation?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” An elimination entry in consolidation is a transaction that eliminates the need for a company to file its financial statements with the SEC.”}}]}

Frequently Asked Questions

Which intercompany transactions should be eliminated?

The following transactions should be eliminated: 1. Company A purchases $100,000 of goods from Company B. 2. Company A sells $100,000 of goods to Company B. The following transactions should be eliminated: 1. Company B purchases $100,000 of goods from Company C. 3. Company A sells $100,000 of goods to Company C. Company C purchases $100,000 of goods from Company D. 4. Company A sells $100,000 of goods to Company D. 4. Company D purchases $100,000 of goods from company E. 2. 3. Company C purchases $100,000 of goods from company D. 4

Why must intercompany transactions be eliminated?

The elimination of intercompany transactions is a key component of the proposed tax reform. The elimination of these transactions will reduce the complexity and compliance costs associated with these transactions. What is the proposed tax reform? The proposed tax reform would reduce the corporate income tax rate from 35% to 20%. The proposal also includes a territorial system for taxation, which would eliminate the current worldwide taxation system.

What is an elimination entry in consolidation?

An elimination entry in consolidation is a transaction that eliminates the need for a company to file its financial statements with the SEC.

Unlock Your Coolest Summer Yet: Dive Into Quality Self-Care Trends

From Novices To Aces: Sales Onboarding Ideal Practices That Work

Empowering Your Community Through a Social Impact Cleaning Business

Winning Strategies for Online Slots: What You Need to Know

Virtual Surgical Training: AI-Driven Simulation for Surgeon Education

Creating Magic Chord D’Paspor Saat Bersamamu A Musical Exploration

Unveiling the Mystery: Exploring and Debunking the Myths of 101 Arti Kedutan

The Thrill of Victory In Dctoto Riding the Wave of Excitement

Revealing Success Through Strategic Goal Setting: A Comprehensive Guide

How Messenger-Based Casinos Help Players Stay Anonymous

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home