3.5 Process Costing

In this post, I’ll outline a process costing methodology for developing a 3.5 process, and show you how to get an idea of the cost of producing the product or service.

In today’s environment, executives are looking for ways to streamline their organizations while preserving the value of their business. As IT processes become more complex, organizations are looking for solutions to manage the costs of their IT operations.

You can increase your profitability by making better use of the thousands of dollars of resources that go into the production of goods and services. Unfortunately, many companies fail to do so effectively because they overlook important details. The challenge of getting precise costing information is often compounded by the fact that all sorts of different costs are involved in making a product.. Read more about process costing exam questions and answers pdf and let us know what you think. Administrative accounts 3.5 Activity-based costing

10.07.2020

Accounting Adam Hill

You then add them to the units already made to get 750,000. This will give you the number of equivalent whole units you have produced.

The production cost report takes the production data and presents it as total amounts spent during the period in question. This report is used by management to analyze production processes and determine if improvements need to be made to achieve maximum efficiency.

1) Does not distinguish between work done in the previous period and in the current period. 2) Mixes the units and costs of the previous and current period. 3) Determines the equivalent production units for the department by adding the number of units transferred from the department to the equivalent units in the completed work in progress inventory.

We will continue the discussion using the weighted average cost method and calculate the cost per equivalent unit. The report is divided into three parts. It compares the total number of units in production with the total number of units released (completed units + units in process). The second indicates the cost per equivalent unit.

Calculation of equivalent production units

However, since the production process takes three weeks, all units produced during the last two weeks of March will be in the warehouse by the end of March. Calculate the costs associated with the paint department’s WIP ending inventory for direct materials, direct labor, overhead, and total. On the previous page, we discussed the physical flow of units (step 1) and the calculation of equivalent units (step 2) using the weighted average method.

You can use the same method to calculate overhead and materials if you know the percentage of completion for each price factor. The production manager was asked to encourage his staff to make as much progress in production as possible to increase the percentage of WIP completed.

This allows managers to see how much of the revenue has been realized in a given period and how much of the revenue is still in progress. It also allows managers to calculate unit costs to help set unit prices for customers.

Therefore, the equivalent units of direct materials will always be higher than the other production costs. Preliminary figures show that pre-tax income for the current year is $1,970,000, which is less than the budgeted $30,000. Companies determine the efficiency of their production processes in various ways. One method is the calculation of equivalent production units.

By the end of the year, a total of 10,000 units remain in the assembly department. Direct materials are 80% complete and direct labor is 40% complete. Calculate the equivalent units in the assembly department for direct materials and direct labor. Each department in the production process must report equivalent units, both completed units and work in progress (WIP).

Weighted average method of equivalent production units

- Therefore, the equivalent units of direct materials will always be higher than the other production costs.

- Preliminary figures show that pre-tax income for the current year is $1,970,000, which is less than the budgeted $30,000.

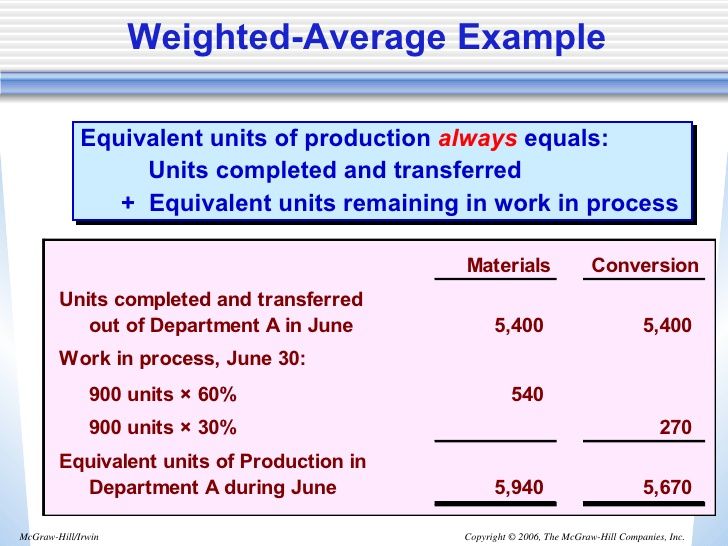

In activity-based costing, the total output of the service over a given period is usually expressed in unit equivalents. In our example, the equivalent output per unit of department X is 5,400 units, which can be used to calculate the unit cost of the department. There is a simple formula used to calculate the equivalent units for these partially completed units. This formula applies not only to materials in current production, but also to labor and overhead costs.

The production cost report is a departmental report that illustrates all the information needed for quick management analysis. Let us assume that a producer permanently uses direct labour in one of its production units.

The weighted average method for calculating equivalent units of production combines the units and costs of the current period with the units and costs of the previous period. Under this method, the equivalent units in the factory are the completed and transferred units plus the equivalent units in the final inventory of work in progress.

Example of equivalent product units

The department started in June with no material in stock, then took off and produced 10,000 units. A thousand units were also launched, but only 30% were completed by the end of June. The production cost report for this service indicates that it produced 10,300 (10,000 + 300) equivalent units in June. The four main steps in allocating costs to units withdrawn from inventory and to units ending with work in progress are formally reflected in the report on the cost of production of goods.

Average unit cost is determined by dividing total cost by the total number of equivalent units to determine the cost of completed and in-process units. For example, if there are 1000 units of work in progress and the company has only spent 40% of the cost to process those units, then you have 400 equivalent units of output. The concept of equivalence units is only used in process costing, because you calculate a unit of equivalence based on a mass quantity of goods.

What are the correct units for direct materials?

The unit equivalent is the expression of the work done by a producer on partly completed units at the end of the reference period. In general, fully completed units and partially completed units are expressed in terms of fully completed units.

Calculate the cost of completed and transferred paint department units for direct material cost, direct labor cost, overhead cost, and total cost. At the end of the year, a total of 6,000 more devices will be tested for quality. Direct materials are 75% and direct labor is 20%. Calculate the equivalent units in the quality inspection department for direct materials and direct labor. Under this method, work in progress and its costs are combined with production and costs of the current period.

Become a PRO or PRO Plus member and get lifetime access to our premium content

Equivalent units are used to report cost of sales. Without this information, you cannot prepare a production cost report. Equivalent completed units Equivalent completed and transferred units 600, rate 600,000 Incomplete production, completion 600, rate 150,000 Equivalent units Equivalent units 750,000 Although 25% of the units are still under construction, 150,000 units can be considered completed.

Calculate the equivalent units for each of the three types of product cost – direct materials, direct labor, and overhead. Let’s say you have enough material to make 600,000 shirts. The table shows the calculation of the equivalent units. For the purpose of applying the FIFO method, only the percentage of opening sections completed during the reference period and the costs incurred for the completion of these sections shall be used.

The cost of production report summarizes the production and cost activities of the processing division for the reporting period. A separate report shall be drawn up for each processing unit. Rounding the cost per equivalent unit to the nearest thousandth of a percent minimizes rounding differences when reconciling the costs considered in Step 2 with the costs considered in Step 4.

The third section illustrates the distribution of costs between completed and in-progress units. The production cost report is a useful tool to support management in the operational planning process. It is very dynamic and adapts to any type of production process. The units currently in production multiplied by the percentage of units completed or in production are called equivalent units. All costs related to the production of the department are taken into account.Over the years, I’ve learned a lot about process costing, and I’ve come to appreciate the many ways it can save costs and increase profits. Here, I want to share a few of my favorite techniques, and explain why I think they’re worth learning.. Read more about cost of production report fifo method example and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How is process costing calculated?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Process costing is calculated by multiplying the cost of each process by the number of units produced.”}},{“@type”:”Question”,”name”:”What is process costing method?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Process costing is a method of cost accounting that uses the direct labor hours required to produce a product as the basis for allocating costs to products.”}},{“@type”:”Question”,”name”:”How is FIFO process costing?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” FIFO process costing is a method of cost accounting that uses the first-in, first-out (FIFO) principle.”}}]}

Frequently Asked Questions

How is process costing calculated?

Process costing is calculated by multiplying the cost of each process by the number of units produced.

What is process costing method?

Process costing is a method of cost accounting that uses the direct labor hours required to produce a product as the basis for allocating costs to products.

How is FIFO process costing?

FIFO process costing is a method of cost accounting that uses the first-in, first-out (FIFO) principle.

A Detailed Guide to Purchasing Wholesale Flowers

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Can PTSD Be Cured? Exploring Treatment Options and Recovery Paths

The 5 Countries for Offshore Manufacturing

BetterThisWorld com: Unveiling New Perspectives

BetterThisWorld.com: Revolutionizing Social Impact Online

Sustainable Investments and Ethical Business Practices for Betterthisworld Money

Betterthisworld Business Social Media Marketing Strategies

Tineco; Changing the Game with the ONE S11 Cordless Vacuum Cleaner

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home