Where Does Accumulated Depreciation Go on an Income Statement?

In simple terms, accumulated depreciation gives a “head start” to a company by allowing it to increase its book value at the expense of its “shareholders”. In other words, companies are allowed to pay themselves a higher rate of interest on their money, which can result in less profits for the shareholders.

It’s been a while since we last covered this subject, but it’s time to revisit. The topic today is how to deal with Accumulated Depreciation on an income statement.

Home Accounting Where is accumulated depreciation reported in the income statement?

13. August 2020

Accounting Adam Hill

Otherwise, accumulated depreciation is equal to the carrying amount of the asset less its residual value. Fixed capital is what financiers call a tangible asset, a capital asset, a physical asset or a depreciable asset. Depreciation is an accounting policy that allows companies to recognize the estimated value of a portion of long-term assets that will be used in the current year. This is a non-cash expense that overshadows earnings, but ties income to expenses in the period in which they are incurred.

Depreciation is recognised in the income statement in the period in which it is incurred. Accumulated depreciation is included in the balance sheet under the respective capitalized assets. The accumulated depreciation balance increases over time by the amount of depreciation recorded in the current period.

Companies that want to increase their profits want to increase their receivables by selling their goods or services. Generally, companies use accrual accounting, which means that when they prepare their balance sheets, they add the balance of receivables to total receipts, even if the money has not yet been received.

- Depreciation expense, on the other hand, is the portion of the company’s fixed asset value attributable to a particular period.

When to use depreciation expense instead of accumulated depreciation

The book value of fixed assets in the balance sheet is the difference between the cost of the asset and the total amount of accumulated depreciation. To allocate the cost of an asset, the company’s bookkeeper debits the depreciation expense account and credits the accumulated depreciation account. The final element is a settlement account that reduces the value of the corresponding fixed assets. Accumulated depreciation can be found directly in the Tangible Fixed Assets account of the balance sheet, also known as the statement of financial position.

Fixed assets are included in the balance sheet, which shows the company’s assets, liabilities and equity over a given period. The equilibrium equation is as follows: Assets equal liabilities plus equity because a company can only finance the purchase of assets with debt and equity. Revenue only increases when receivables are converted into cash receipts through collections. Sales are the total sales of the company before expenses.

Depreciation expenses are charged to the income statement. Here the accumulated depreciation is combined with the income statement – another name for the profit and loss account. Capitalised tangible fixed assets are also included under fixed assets, with the exception of the portion to be charged to the result or depreciated in the current year. Capitalized assets are fixed assets that can be used for more than one period.

In the trial balance, accumulated depreciation is an offsetting account for property, plant and equipment. Impairment is a method of recording changes in the value of an asset. Depreciation also affects corporate tax and is reflected in your tax return.

Accumulated depreciation

You record the depreciation expense in the income statement and report the accumulated depreciation as a settlement account in the balance sheet. Accumulated depreciation is the total of depreciation expense since the acquisition and use of the asset. The accumulated depreciation account is an offsetting account on a company’s balance sheet, meaning that it has a credit balance. It is presented in the balance sheet as a reduction in the gross amount of tangible fixed assets. Accumulated depreciation is the total amount by which an entity depreciates its assets, and depreciation expense is the amount by which the entity depreciates its assets in a period.

No, it is not common for the balances of the two accounts to be the same. Depreciation expense is recognized in the income statement; accumulated depreciation is recognized in the balance sheet.

For accounting purposes, depreciation expense is debited and accumulated depreciation is credited. When depreciation is recorded in the general ledger, the company debits the depreciation expense and credits the accumulated depreciation.

Is accumulated depreciation an asset of the entity?

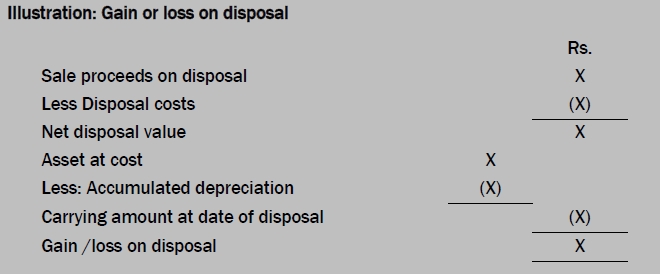

Accumulated depreciation is recorded in the balance sheet directly below the corresponding line item for fixed assets. The carrying amount of an asset is its historical cost less accumulated depreciation.

Accumulated depreciation has a credit balance because it combines the amount of accumulated depreciation expense on an asset. This account is related to the capital asset item on the balance sheet, so the sum of these two accounts represents the net book value of the capital assets. Over time, the amount of accumulated depreciation will increase as property, plant and equipment is depreciated, resulting in a further decrease in the carrying amount of the asset. Accumulated depreciation is the sum of depreciation expense over several years.

How does proportionality affect the impairment of assets?

Whenever an entity recognises a write-down as an expense in the income statement, it increases the accumulated depreciation for that period by the same amount. Consequently, the entity’s accumulated depreciation increases over time as the entity’s assets continue to be depreciated. Accumulated depreciation is the total depreciation of an asset up to a certain point.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”Does Accumulated Depreciation go on an income statement?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” No, accumulated depreciation is a non-cash expense that is not recorded on the income statement.”}},{“@type”:”Question”,”name”:”Where do you put Accumulated depreciation on a balance sheet?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Accumulated depreciation is put on the balance sheet as an asset.”}},{“@type”:”Question”,”name”:”How is depreciation shown on income statement?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Depreciation is shown on the income statement as a reduction in the value of assets.”}}]}

Frequently Asked Questions

Does Accumulated Depreciation go on an income statement?

No, accumulated depreciation is a non-cash expense that is not recorded on the income statement.

Where do you put Accumulated depreciation on a balance sheet?

Accumulated depreciation is put on the balance sheet as an asset.

How is depreciation shown on income statement?

Depreciation is shown on the income statement as a reduction in the value of assets.

4 Benefits of Document Digitizing Services for Businesses

Personalized Engagement Rings: Crafting a Unique Symbol of Your Relationship

Why Drink Gaming Energy Drinks & How to Choose the Right Ones

Your Guide to Elevating Your Appearance

Ace Your Project: Local Student Tips Revealed!

Gaming Evolution: The Transition From Real-World to Online Casinos

10 Biggest Cryptocurrency Exchanges of 2024

Excitement at Ovo188 Login Top Online Casino

The Features and Community of Indobolamas88

How to Identify and Choose Trusted Online Casinos in Malaysia

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home