What’s the Difference Between Amortization and Depreciation in Accounting?

Amortization and depreciation are two important accounting terms that are used to account for the amount of a long-term asset or liability used to compute its current and future book values over time. Understanding these terms is important as they are widely misunderstood and incorrectly applied, which can lead to mistakes in financial statement presentation, incorrect conclusions about a company’s financial health, and inaccurate judgments about the value of a company’s assets and liabilities. Additionally, there are some accounting challenges that arise in the use of these terms, which can lead to additional confusion.

The two are often confused, and that’s because they are very similar. Depreciation is the equivalent of amortization in financial terms. These terms are both used to describe the gradual reduction of the asset value of an asset over its useful life.

Accounting Home What is the difference between depreciation and amortization in accounting?

15. October 2020

Accounting Adam Hill

Secondly, redemption shortens the maturity of the bond, making it less sensitive to interest rate risk than other non-redeemed bonds with the same maturity and coupon. This is because interest payments decrease over time, resulting in a lower weighted average maturity (WAM) of the cash flows associated with the bond. If the borrower were to make fully redeemed payments, he or she would pay $1,266.71, as shown in the first example, and this amount would increase or decrease as the interest rate on the loan changes.

If regular payments are made on time, the loan or mortgage will be paid off when due. At the end of the first year, you have made 12 installment payments, most of which are interest payments, and only $3,406 in principal has been paid off, the balance of the loan is $396,593. The following year, the monthly payments remain the same, but the principal increases to $6,075. We now turn to year 29, where $24,566 (almost the entire annual payment of $25,767.48) is used to pay off the principal. You can easily find free mortgage or repayment calculators online to help you make these calculations quickly.

This term is usually used for mortgages; commercial loans with negative repayment are called PIK loans. Regular mortgage payments reduce your principal and interest. With a 15-year fixed rate mortgage, the loan is fully paid off after 15 years. A 30-year fixed rate mortgage is fully repaid at the end of 30 years through periodic payments.

What is a direct mortgage?

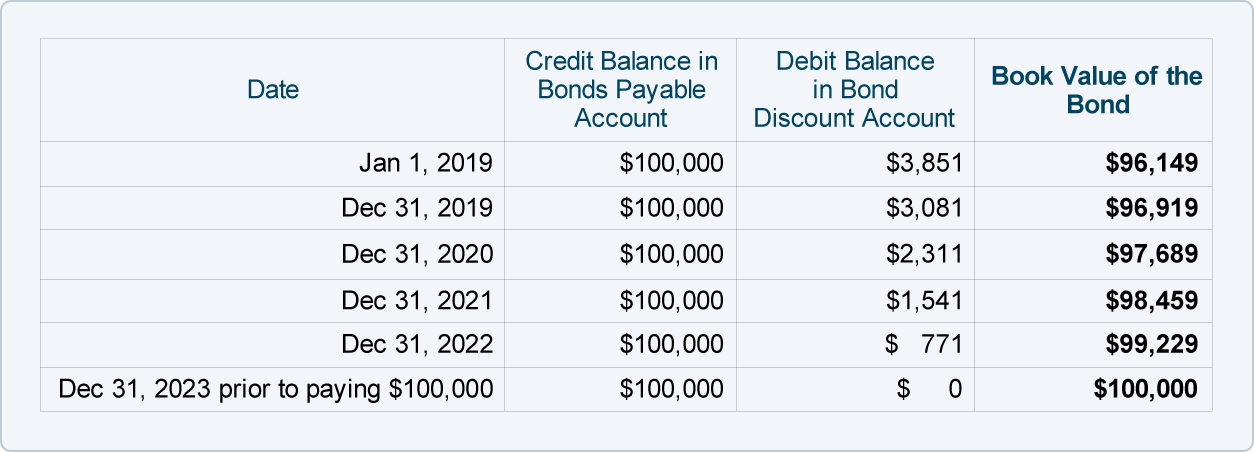

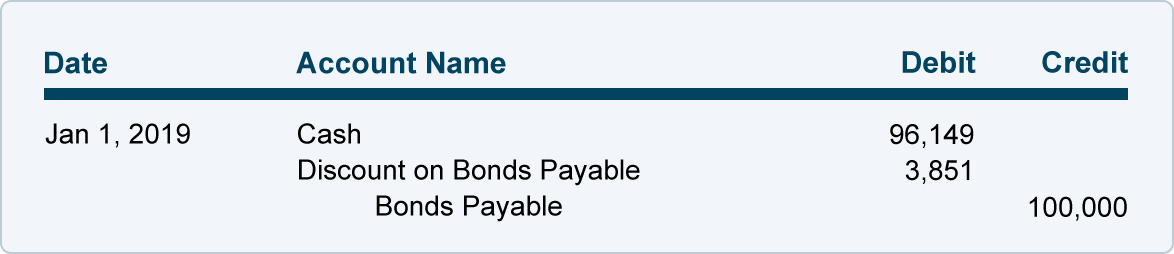

Straight-line depreciation is still the easiest way to book discounts on or premiums for bonds. Under the straight-line method, the bond premium or discount is amortized in equal amounts over the life of the bond. Premiums are amortized in a similar manner.

For a loan with monthly payments, divide the result by 12 to get the monthly interest rate. The interest is deducted from the total monthly payment and the remaining amount is used to repay the principal.

The amount of principal due in a given month is the total monthly payment (fixed amount) less the interest payment for that month. The following month, the loan balance is calculated as the previous month’s balance minus the last payment on the principal debt. Under the amortisation method, the reduced amount (the difference between the interest and the repayment) is then added to the total amount owed to the creditor. This practice should be agreed upon before the payment is reduced to avoid delays in payment. This method is usually used in the introductory phase, when the repayments are higher than the interest and the loan becomes self-repaying.

Creating a repayment plan is relatively easy if you know your monthly loan payments. Starting with the first month, take the total amount of the loan and multiply it by the interest rate of the loan.

Personal loans that you get from a bank, credit union or online lender are usually also paid off loans. They often have a three-year term, fixed interest rates and fixed monthly payments. These loans are often used for small projects or debt consolidation. Deleveraging affects two fundamental risks of bond investments.

When paying a mortgage and a car loan, a larger portion of the fixed monthly payment is initially spent on interest payments. With each subsequent payment, an increasing percentage of the payment goes towards repayment of the loan amount. Depreciation can be calculated with most modern financial calculators, spreadsheets like Microsoft Excel, or online depreciation tables. This table is very useful for correctly booking the interest payments and the loan repayments.

Repayment is the reduction of debt over time by paying the same amount each period, usually monthly. In case of repayment, the amount to be paid consists of the repayment of the principal and the interest on the debt.

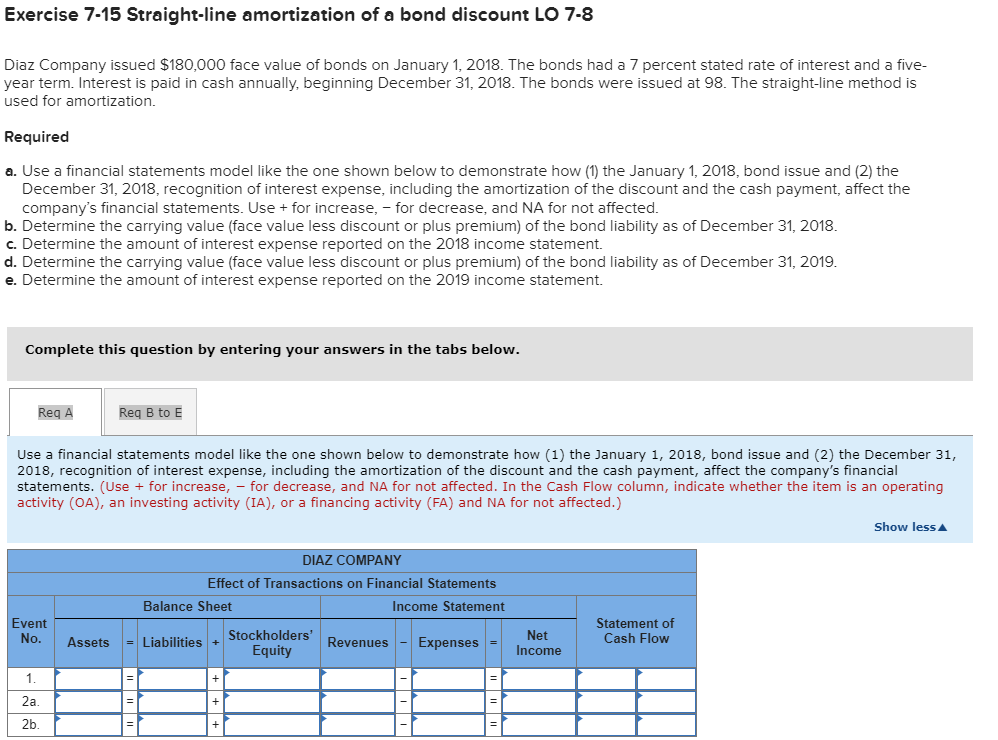

How the liability should be accounted for under the straight-line method of annual depreciation and the effective interest method, and the effect of selecting one method over the other.

- Repayment is the reduction of debt over time by paying the same amount each period, usually monthly.

A fully repaid payment is a form of periodic debt repayment. If the borrower makes the payments according to the repayment schedule, the debt will be repaid in full at the end of the fixed term. If it’s a fixed rate loan, each fully repaid payment is an equal amount.

However, if the loan is structured so that the borrower only pays the interest during the first five years, the monthly payment for that period will only be $937.50. As a result, his payments could increase to $1,949.04 after the phase-in period ends. By not making fully repaid payments at the beginning of the loan, the borrower essentially commits to making larger fully repaid payments later. Repayment is the process by which a debt is paid off over time through regular payments of interest and principal, sufficient to repay the loan in full at maturity.

The principal payable over the life of a loan or bond repaid is allocated according to an amortization schedule, usually by calculating equal payments over the life of the loan or bond. This means that in the first few years of the loan, the interest portion of the debt service will be higher than the principal portion. However, as the loan is repaid, the portion of each payment that goes to interest payments decreases and the principal payment increases.

However, each payment represents a slightly different percentage of interest and principal. A redemption bond differs from an early redemption loan or a bullet loan, where the majority of the principal is not due until maturity. To illustrate a fully amortized payment, let’s say a man has a 30-year mortgage with a fixed interest rate of 4.5% and monthly payments of $1,266.71. Since these payments are fully amortized, if the borrower makes them each month, they will repay the loan at the end of the term.

Linear Mortgage Calculation

A repayment schedule is used to determine the current balance of a loan, such as a mortgage or car loan, by making payments in installments. A repayment table gives you the most basic information about your loan and how you will repay it. It usually contains a complete list of all the payments you will have to make during the term of the loan. Each payment in the schedule is broken down into the interest portion and the principal portion of the payment.

Is depreciation always straight-line?

The straight-line method is the simplest way to depreciate a bond or loan, because it allocates an equal amount of interest to each accounting period over the life of the debt. The straight-line depreciation formula is calculated by dividing the total amount of interest by the number of periods during the life of the debt.

What is straight-line depreciation?

When the principal is repaid, interest is payable on the remaining principal at a lower rate. Over time, the interest portion of each monthly payment decreases and the principal portion increases. Amortization is an accounting method that periodically reduces the carrying amount of a loan or an intangible asset over a period of time. First, repayment is used in the repayment of debts through regular payments of principal and interest over time.

The calculations for a grace loan are similar to those for an annuity, using the time value of money, and can be done quickly with an amortization calculator. A depreciated bond is a bond whereby the principal (nominal value) is paid periodically together with interest expenses during the term of the bond. A common example is a fixed rate home loan, where the monthly payment remains constant over a period of, say, 30 years.

Gather the necessary information to calculate the loan repayment. To calculate the repayment, you will also need the term of the loan and the amount of the repayment for each period. Most NegAm loans today are tied to the monthly Treasury average, which is the monthly adjustments to that loan. There are also hybrid ARM loans, where there is a period of fixed payments for a few months or years and then an increasing cycle of changes, e.g., “I’m not going to be able to pay you. Fixed for six months, then adjustable monthly. Debt repayment is the process of reducing the balance of the debt by repaying the principal and interest according to a schedule.

In the second month, do the same thing, but start with the first month’s loan balance instead of the original loan amount. At the end of the specified credit period, the principal amount must be zero.

When you take out a loan with a fixed interest rate and a fixed repayment period, you will normally receive a repayment schedule for the loan. If you know how to calculate the repayment schedule for a loan, you will be in a better position to consider important steps, such as… B. Make extra payments to pay off your loan faster. For monthly payments, the interest payment is calculated by multiplying the interest rate by the loan balance and dividing it by twelve.

Short-term loans have a lower interest rate because they are repaid over a shorter period of time. Repayment is the process by which a loan (such as a home or car loan) is broken down into a series of fixed payments. Although each monthly payment remains the same, the payment is made up of parts that change over time. A portion of each payment is used to pay the interest (what your lenders paid for the loan) and to reduce the balance of the loan (also called repayment).{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What expenses can be amortized?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Expenses that can be amortized are those that are paid for over a period of time. These expenses include: Interest on a loan Insurance premiums Interest on a mortgage Interest on a credit card Interest on a car loan Interest on a student loan Interest on a home equity loan Interest on a personal loan Interest on a line of credit Interest on a revolving credit account Interest on a savings account Interest on a certificate of deposit Interest on a money market account Interest on a mutual fund Interest on a bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond”}},{“@type”:”Question”,”name”:”What is amortization with example?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The amortization is the process of paying off a loan or debt, with the amount of the loan or debt being reduced over time.”}},{“@type”:”Question”,”name”:”Are intangible assets depreciated or amortized?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Intangible assets are amortized.”}}]}

Frequently Asked Questions

What expenses can be amortized?

Expenses that can be amortized are those that are paid for over a period of time. These expenses include: Interest on a loan Insurance premiums Interest on a mortgage Interest on a credit card Interest on a car loan Interest on a student loan Interest on a home equity loan Interest on a personal loan Interest on a line of credit Interest on a revolving credit account Interest on a savings account Interest on a certificate of deposit Interest on a money market account Interest on a mutual fund Interest on a bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond Interest on a municipal bond Interest on a corporate bond Interest on a treasury bond

What is amortization with example?

The amortization is the process of paying off a loan or debt, with the amount of the loan or debt being reduced over time.

Are intangible assets depreciated or amortized?

Intangible assets are amortized.

7 Unusual Facts About Indonesia

The Future Trajectory of Jackpot Gaming Innovations

How to Determine Reliability of Individual Proxies

How to Choose the Right CBD Vape Pen for Your Needs: A Purchaser’s Guide

How To Choose a Wedding Ring to Match a Profession

Strategies for Personal Finance Growth: Exploring BetterThisWorld Stocks

Explore the Strategic Advantages of Betterthiscosmos Posts

Mastering YY4D Login: A Step-by-Step Guide to Secure User Experience

Smart Spending, Stylish Living: Finding Discounts on Luxury Brands

Exploring Btwradiovent Event by Betterthisworld: BetterThisWorld’s Revolutionary Event on Digital Broadcasting and Social Reform

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home