What Percentage of Expenses Should Payroll Be?

This article will address how much of your business expenses should be deducted from your paycheck, and why. Payroll deductions are a key step in the calculation of your business expenses as they help you to maintain healthy cash flow. In fact, if your business expenses were not deducted from your paycheck, you will not be able to operate your business as you need to.

The “right” percentage of payroll expenses for an average small business is a controversial topic. Some say it should be around 50%, while others say it should be as low as 30%. Others still say it should be much lower.

Accounting Home What percentage of expenses should be allocated to payroll?

10. September 2020

Accounting Adam Hill

What is the percentage of the fee?

Calculate the overhead rate by dividing the total overhead amount by the number of individual work hours. For every hour it takes to make a product, you have to spend $2.50 on overhead.

These costs are considered overhead because they are not directly attributable to a specific function of the organization and do not generate profit. Instead, these costs simply take on the role of supporting all other business functions. Overhead costs are all costs included in the income statement except direct labour costs, direct material costs and direct labour costs. Overhead costs include accounting, advertising, insurance, interest, legal fees, labor costs, rent, repairs, supplies, taxes, phone bills, travel costs and utilities.

In addition, property taxes do not change based on business profits or sales and will likely remain the same unless the state’s administration changes. Fixed production costs are all the costs a company incurs on the physical platform on which a product or service is created. The difference between production overhead and administrative overhead is that production overhead is classified in the factory or office where sales are made. While administrative overheads are generally classified as back office or back office costs. Although in some cases two physical buildings may overlap, it is the use of overhead that separates them.

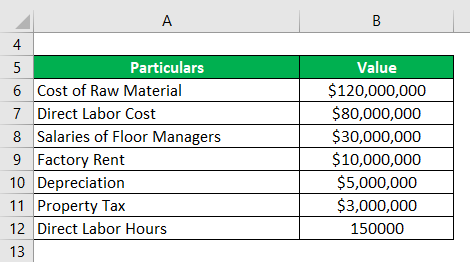

The usual basis for the allocation is the number of direct labour hours spent on the product or the number of machine hours used to produce the product. The amount of deduction per unit of activity is called the overhead rate. The overhead rate (or tariff) is sometimes seen as a puzzling percentage applied to a contractor’s labor costs, often based on comparable figures from the previous year. This year, Kline expects overhead costs of $800,000 to $200,000 in the cutting and polishing department and $600,000 in quality control. The cutting and polishing department expects to use 25,000 machine hours and the quality control department expects to use 50,000 direct labor hours during the year.

Distribution tariff

While these costs are necessary in most cases, they can sometimes be avoided or reduced. Administrative overhead includes items such as utilities, strategic planning, and various support functions.

- Overhead costs are costs that, unlike operating costs such as raw materials and labour, cannot be easily traced or identified by a specific cost object.

- In business, overhead or indirect costs refer to the ongoing costs of doing business.

- Overhead costs can therefore not be directly related to the products or services offered and therefore do not generate a direct profit.

Overhead absorption is based on a combination of overhead rates and the use of an allocation basis on the cost object. For example, the allocation of product overhead may be based on an overhead rate of $5.00 per hour worked, which may be modified by changing the number of hours worked or the overhead amount in the cost pool.

This does not apply if the company has its own in-house lawyers and audit plans. Due to regulatory requirements and the annual audits required to ensure a satisfactory working environment, these costs are often unavoidable. Since these costs do not necessarily contribute directly to sales, they are considered as indirect overheads.

A problem often arises if this rate is not monitored or reviewed annually to verify that it accurately reflects the company’s actual overhead costs. When this happens, costs may be over- or under-allocated, distorting financial results and affecting the ability of owners and financial managers to properly manage the business. These may include rent or mortgage charges, depreciation of assets, salaries and wages, membership and registration fees, legal fees and accounting fees. The fixed cost amounts remain the same whether the company makes more revenue or incurs more losses in that month. Payroll costs, including the outsourcing of payroll services, are included in fixed costs.

The approach is similar to the plant-wide approach except that cost pools are created for each department rather than the entire plant and a separate predetermined overhead rate is established for each department. Instead, they are distributed among the different cost pools of the various departments. This approach may use different allocation bases for the different departments, depending on what determines the overhead costs of each department. For example, SailRite’s hull manufacturing department may determine that overhead costs are more attributable to machine use than labor, and therefore decide to use machine hours as the basis for allocation. The assembly department may find that overhead costs are more related to labor activities than to machine use, and therefore decide to use labor hours or labor costs as the basis for allocation.

This includes office equipment such as printer, fax machine, computer, refrigerator, etc. These are devices that do not lead directly to sales and profits, as they are only used for the support functions they can provide to the business.

The overhead absorption rate is calculated to include overhead costs in the cost of goods and services. It is used to determine the amount to be written off for labor, materials and other production overhead costs in work in progress.

In business, overhead or indirect costs refer to the ongoing costs of doing business. Overhead costs are costs that, unlike operating costs such as raw materials and labour, cannot be easily traced or identified by a specific cost object. Overhead costs can therefore not be directly related to the products or services offered and therefore do not generate a direct profit. Nevertheless, overhead costs are still essential to the operation of a business, as they support the performance of profitable activities.

For example, if an enterprise’s activity is labor-intensive, such as casting concrete, the best allocation method would be direct labor costs. In addition, health insurance, payroll taxes or benefits related to direct employment that cannot be attributed to a specific job should be included in indirect costs and allocated to jobs. If an administrative assistant was involved in construction activities for part of his time, the costs associated with that employee for that part of his time should be included in indirect costs. Assume that Kline allocates overhead costs using the plant-wide method and that the basis for the allocation is direct labor costs. Calculate the percentage the company uses to allocate overhead.

Direct material costs are one of the most important components of production costs. In this method, the absorption coefficient is based on the direct material cost. To calculate this figure, divide the overhead cost by the estimated or actual direct material cost. There are two main methods for estimating the allocation of overhead costs, which are sometimes mixed using either direct labour costs or direct material costs. In assessing the most appropriate method for a contractor, the starting point should be the most critical element of the construction activity – labor or materials.

What is the distribution ratio?

These are the total costs of formulating policies, planning and controlling the activities of an organization and motivating the staff to achieve the objectives. These costs are not directly attributable to activities or functions of production, sale, distribution, research or development. In the soft drink bottling plant scenario above, the lease payments for the plant are still due even though the plant has no ongoing production. Similarly, the company continues to incur other distribution costs, such as. B. Insurance benefits and salaries of administrative and managerial personnel.

Although these expenses are incurred regularly and sometimes without prior preparation, they are usually one-time payments that do not exceed the company’s travel and entertainment budget. Make a complete list of the company’s indirect costs, including items such as rent, taxes, utilities, office equipment, facility maintenance, etc. Direct costs related to the production of goods and services, such as. B. Labor and raw material costs are not included in overhead.

Accounting tools

What is overhead allocation?

The payout rate is the percentage of the investor’s money or capital contribution that is allocated to the final investment. The allocation ratio generally refers to the amount of capital invested in a product less the costs incurred in the investment transaction.

There are two types of overhead costs: administration costs and production costs. Production overheads are all costs incurred in the factory that are not direct costs. To calculate overhead, add up all the ongoing costs that keep your business running but are not related to generating revenue. These are indirect costs such as administration costs, sales and marketing costs and production costs. You can assign overhead to any reasonable figure, as long as it is applied consistently across all reporting periods.

Overhead costs are other costs not related to labour, direct materials or production. These are more static costs related to general business functions, such as salaries for accounting staff and installation costs.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What percentage of costs are wages?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Wages are the largest component of costs.”}},{“@type”:”Question”,”name”:”What percentage should business expenses be?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A business expense is a cost that is incurred by a business to conduct business operations. Business expenses are deductible from gross income. The percentage of business expenses that are deductible is between 20% and 50%, depending on the type of business. A business expense is a cost that is incurred by a business to conduct business operations.”}},{“@type”:”Question”,”name”:”How do you calculate payroll percentage?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” To calculate payroll percentage, divide the total payroll for the year by the total sales for the year.”}}]}

Frequently Asked Questions

What percentage of costs are wages?

Wages are the largest component of costs.

What percentage should business expenses be?

A business expense is a cost that is incurred by a business to conduct business operations. Business expenses are deductible from gross income. The percentage of business expenses that are deductible is between 20% and 50%, depending on the type of business. A business expense is a cost that is incurred by a business to conduct business operations.

How do you calculate payroll percentage?

To calculate payroll percentage, divide the total payroll for the year by the total sales for the year.

The Future of Online Gambling: Instant Withdrawals in Singapore

Spinning the Reels: A Comprehensive Guide to Online Slots

Revealing Success Through Strategic Goal Setting: A Comprehensive Guide

Jumpstart Your Week: Tips to Keep You Motivated for Monday Workouts

Top 5 Must-Read Personal Finance Books for Achieving Financial Freedom

Mobile . de: Navigating Germany’s Premier Online Vehicle Marketplace

Pamper Your Pet: Fressnapf. de/gewinnen

Markt. de Login: Quick Guide to Access Your Account

Understanding Player Preferences In Online Game Theme Selection

Unveiling The Most Popular Picks Ideal Electric Scooter For Every Rider

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home