What are Period Costs?

Period costs refer to the costs of a woman’s period, which includes specific costs that are associated with menstruation. Period costs are usually associated with health care costs, which may include physician visits, prescription medications, and hospitalization services. If a woman does not have health insurance, her period costs may be more expensive since her health insurance plan usually does not cover menstrual health care services.

According to the Bureau of Labor Statistics in the United States, the average woman in America spends $250 per year on disposable menstrual products. That’s a lot of money, and the hassle of storing and disposing of pads and tampons can be a hassle for many women. Many women prefer to just use a tampon and let it sit in place, but that isn’t always the best option. Although tampons are a good option for many women, they aren’t for everyone. If you’ve never used a tampon before, you should do some research on the matter and make a choice that will fit your personal needs and preferences. However, if you’ve used tampons before, you might

Accounting Home What is an accrual expense?

14. September 2020

Accounting Adam Hill

When an item is sold, its cost is removed from inventory and recognized in the income statement as cost of goods sold. Other examples of recurring costs are marketing costs, rent (not directly related to the production facility), office depreciation and indirect labour costs. In addition, interest expense on the entity’s debt is recorded as an expense for the period.

These may include rent or mortgage charges, depreciation of assets, salaries and wages, membership and registration fees, legal fees and accounting fees. The fixed cost amounts remain the same whether the company makes more revenue or incurs more losses in that month.

Overhead costs also include the salaries of personnel assigned to the production unit but not directly involved in production, such as. B. Managers and cleaners. Other overhead costs include utilities, building depreciation or rental, quality control, and indirect consumables such as cleaning supplies and trash cans. If your small business produces different types of products in one operation, these costs should be properly allocated to the different product lines. In business, overhead or indirect costs refer to the ongoing costs of doing business. Overhead costs are costs that, unlike operating costs such as raw materials and labour, cannot be easily traced or identified by a specific cost object.

Examples of industries which may not report a cost of sales (COGS)

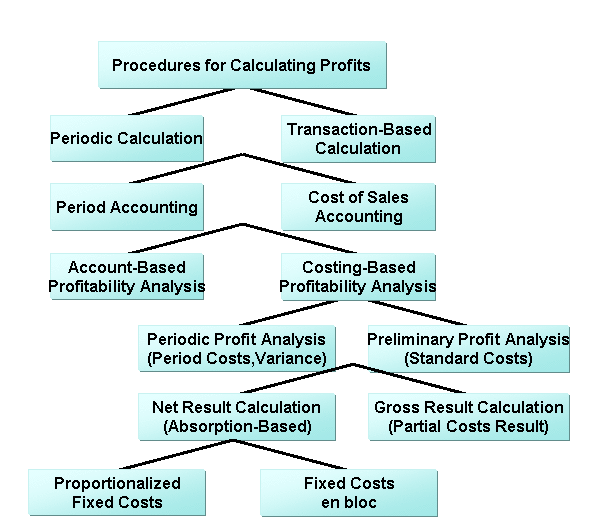

Period costs are usually related to the sales function or general administration of the business. Period costs are recognized as an expense in the accounting period in which they 1) best match revenue, 2) expire, or 3) in the current accounting period. In addition to selling and general administrative expenses, the majority of interest expense is attributable to period expenses. Cost of goods sold (COGS), also known as cost of sales or cost of services, shows how much it costs to produce your products or services. Cost of goods sold includes the direct costs of materials and labor required to produce each good or service sold.

Examples of recurring expenses are selling and administrative expenses. Periodic costs are always charged to the income statement in the period in which they are incurred.

Product costs

Should this spent money be immediately recognized in the income statement? This cost price represents an asset on the balance sheet (inventory). These inventories remain under assets until the goods are sold. At that time, the inventory is eliminated and its cost is transferred to cost of goods sold in the income statement. Cost of goods sold (COGS) is the direct cost of producing the goods sold by the company.

For example, a car manufacturer’s manufacturing costs include the cost of materials for the parts that go into the vehicle and the labor costs for assembling the vehicle. The costs of transporting the vehicles to the dealers and the labour costs of selling the vehicle are excluded. Recurring costs can be distinguished from product costs, which can be directly attributed to production.

Product costs exist for ongoing contractual services, which may include raw materials, direct labour, delivery costs and commissions paid to sales personnel. However, these items cannot be reported as operating expenses without a product being physically produced for sale. The IRS website even gives some examples of personal service companies that do not calculate COGS on their income statements.

Overhead costs can therefore not be directly related to the products or services offered and therefore do not generate a direct profit. Nevertheless, overhead costs are still essential to the operation of a business, as they support the performance of profitable activities. For example, overhead costs such as factory rent allow workers to produce products that can then be sold at a profit.

Some materials used in the manufacture of a product have minimal cost, such as. for example. screws, nails and adhesives, or are not part of the final product, such as. B. Lubricant for machinery and adhesive tape used in painting. These materials are called indirect materials and are accounted for as indirect production costs. Indirect production costs include general material and manufacturing costs and all other production costs. Equipment depreciation, equipment rental, equipment insurance, equipment property taxes, and equipment utilities are all examples of indirect production costs. Direct material costs, direct labor costs, and indirect production costs are collectively referred to as production costs.

The cost of a product includes the direct labour costs – for example the work of an assembler – as well as the materials used directly in manufacturing the product and general production costs. The cost of goods sold is recorded in an inventory account and weighted by the sales proceeds to obtain an estimate of the profit on the sale. Product costs relate to the products manufactured and sold by the company. Product costs are defined as all costs incurred to acquire or produce the final product. Examples of production costs are the cost of raw materials, direct labour and overhead.

- For example, a car manufacturer’s manufacturing costs include the cost of materials for the parts that go into the vehicle and the labor costs for assembling the vehicle.

Accounting tools

The actual cost method allows you to determine the total value of your small business’s output and unit costs based on the actual costs incurred during the period. Knowledge of production costs can help you price your products and set your budget for your small business. Recurring costs are costs that cannot be directly attributed to the production of the final product.

This amount shall include the cost of materials and labour used directly in the manufacture of the product. Indirect costs, such as B. The costs of distribution and sales personnel are not included.

What is the difference between cost of goods sold and cost for the period?

Period costs are all costs that cannot be capitalized as prepaid expenses, inventories or property, plant and equipment. Period costs are more closely related to the passage of time than to the transaction event. Instead, they are usually disclosed in the selling, general and administrative expenses section of the income statement.

Why is the distinction between product costs and period costs important?

Direct production costs are taken into account by including them in the cost price of the goods produced, while periodic costs are booked as expenses. By analogy, a manufacturer invests in direct materials, direct labor, and general production costs.

Accounting policies II

Before the products are sold, these costs are recorded in the inventory accounts of the balance sheet. Product costs are also called inventory costs. When products are sold, these costs are recognized in the income statement as cost of goods sold. Inventories that are sold are included in the income statement in the cost of sales. Opening stock is the remaining stock of the previous year, i.e. the goods that have not been sold in the previous year.

In addition to direct material and manufacturing costs, overhead costs are also a very important cost component. Recurring expenses are expenses that are recognized in the income statement without reference to revenue. As this is not a product cost, the cost for the period is not included in the cost of inventory. Instead, period costs are called period expenses because they are presented in the income statement as selling, general and administrative expenses (SG&A) or interest expense.

Payroll costs, including the outsourcing of payroll services, are included in fixed costs. Labor costs, such as B. Employee hours not related to direct production or manufacturing activities are also fixed costs. In management accounting, product costs are the costs required to manufacture a product. Production costs equal the sum of your direct material costs, your direct labor costs, and your indirect production costs.

The cost of selling a product is an operating cost (period-specific cost) and is not part of the indirect production cost because it is not incurred in producing the product. Product costs include direct material costs, direct labour costs and attributable indirect production costs. Examples of recurring costs include general and administrative expenses such as rent, depreciation of offices, office supplies and utilities. As shown in the income statement above, salaries and benefits, rent and overhead, depreciation and interest are all expenses in the period in which they are incurred. Conversely, the cost of goods sold is recognised as an expense in the income statement when the inventory is sold.

Overhead costs or business, general and administrative expenses (B & G) are considered as expenses for the period. Selling, general and administrative expenses include office, sales, marketing and general administrative expenses. Direct materials are those materials (including purchased parts) used in the manufacture of a product that can be directly associated with the product.

Any additional production or purchases by the producing or retailing company will be added to the original stock. At the end of the year, unsold products are deducted from the initial stock and additional purchases. The final figure resulting from this calculation is the cost of sales for the year. Consequently, the cost of the period cannot be attributed to either production or inventory.

Product costs include the cost of manufacturing or delivering the product. If the product is not sold, the value of the product is booked as stock in the balance sheet.

Costs that form part of the cost price of goods sold are called product costs. These costs arise during the production process, either directly in the form of material and labour costs, or indirectly in the form of overheads. For this purpose, the costs of the products are deducted from the conversion costs and therefore only booked as costs when the products are sold. Recurring costs, also known as periodic costs, are costs incurred by the enterprise that cannot be directly attributed to the production of a result. Because of the indirect link between the cost of the period and inventories, the cost of the period cannot be included in the cost of goods sold.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”Which two examples are period costs?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A. Rent B. Electricity C. Car insurance C. Car insurance”}},{“@type”:”Question”,”name”:”Are salaries period costs?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Salaries are not period costs.”}},{“@type”:”Question”,”name”:”Are period costs the same as operating expenses?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” No, operating expenses are the costs of running an activity, while period costs are the costs of running a business for a specific period of time.”}}]}

Frequently Asked Questions

Which two examples are period costs?

A. Rent B. Electricity C. Car insurance C. Car insurance

Are salaries period costs?

Salaries are not period costs.

Are period costs the same as operating expenses?

No, operating expenses are the costs of running an activity, while period costs are the costs of running a business for a specific period of time.

A Detailed Guide to Purchasing Wholesale Flowers

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Can PTSD Be Cured? Exploring Treatment Options and Recovery Paths

The 5 Countries for Offshore Manufacturing

BetterThisWorld com: Unveiling New Perspectives

BetterThisWorld.com: Revolutionizing Social Impact Online

Sustainable Investments and Ethical Business Practices for Betterthisworld Money

Betterthisworld Business Social Media Marketing Strategies

Building Your Crypto Knowledge: Must-Read Books and Resources for Enthusiasts

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home