What are operating expenses?

The term “operating expenses” refers to the expenses that you will incur in the normal running of your business. This is distinct from your capital expenses, which will be incurred in the expansion of your business. For example, if you offered an internet-based business telephone service, then your operating expenses would include the monthly telephone costs, but not equipment—your capital expenses are the telephone equipment.

Operating expenses are the expenses that a company incurs in the process of running day to day operations of the business. Operating expenses are the expenses that a company incurs in the process of running day to day operations of the business. They include all the bills that a business incurs in running its daily business. They include all the bills that a business incurs in running its daily business. They include salaries, rent, utilities, marketing, paper, phones, insurance, legal, and everything else that a company has to pay for in order to operate.

Accounting Home What are operating expenses?

8. September 2020

Accounting Adam Hill

Operational and non-operational expenditure

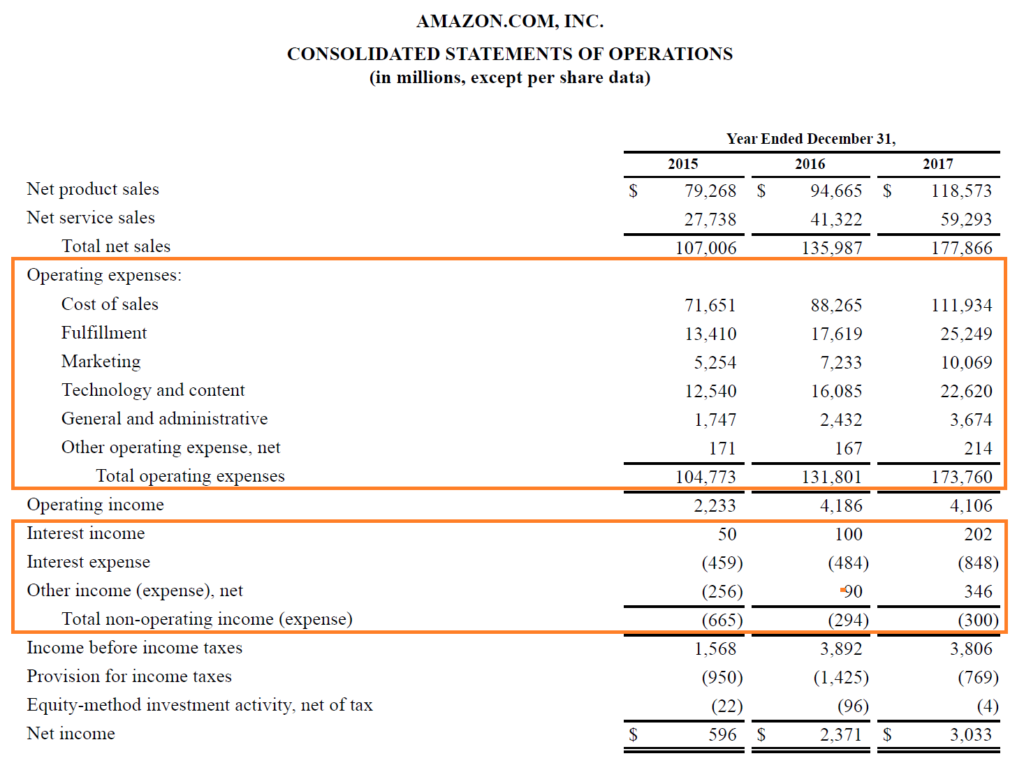

Each year, companies generate income or incur losses by maintaining cash accounts with banks. Banks typically pay companies interest on their account balances and in some cases companies receive dividends or other income from investments in the securities they hold.

Accountants sometimes eliminate non-operating expenses to examine business performance, ignoring the effects of financing and other irrelevant issues. In some cases, non-operating items are identified as non-core revenues, whereas the entity’s ordinary activities are regarded as primary.

What is included in the operating costs?

Operating expenses are incurred in the normal course of business and include rent, equipment, inventory, marketing, salaries, insurance and research and development funds. Operating expenses are necessary and mandatory for most businesses.

Non-operating expenses are operating costs that are not related to the core business. The most common types of non-operating expenses are interest expense and losses on the sale of assets. Accountants sometimes delete non-operating expenses and revenues to examine the performance of the company, ignoring the effects of financing and other irrelevant matters.

What are examples of business expenses?

Costs incurred in day-to-day operations that cannot be attributed directly to production. Operating expenses include salaries, sales commissions, employee benefits and pension contributions, transportation and travel, depreciation, rent, repairs and taxes.

In accrual accounting, reconciliation is NOT based on the date the expense is paid. Non-operating expenses are deducted from operating revenues and recognized at the end of the company’s income statement.

When your business is healthy and successful, the value of your business increases with the money you spend on salaries, wages and operating expenses. The direct labor included in the cost of goods sold must be used to make products that you can sell for more than the cost of the materials and labor used to make them. These sales typically become assets that increase the net worth of your business. Wages, salaries and expenses are important parts of the income statement, which lists everything you earned and spent in a given period, and then calculates the difference as net profit or net loss.

Non-operating items in the income statement include anything unrelated to the company’s main activity of generating profit, such as. B. Interest, dividends, capital gains or losses. Income statements can give investors crucial insight into the health of a company if they know how to read them. It is important to include both operating and non-operating items in the income statement, as a company may appear profitable in its core business yet incur significant losses due to non-operating expenses. It is important for most individual investors to understand certain items in the non-operating income statement and the risks associated with them. Insurance costs, personnel costs, advertising costs, interest costs are costs that correspond to the period in the header of the income statement.

- The company begins the income statement with the top line of sales.

- When you look at a company’s income statement from top to bottom, operating expenses are the first expense item, just below revenue.

In some cases, taxes are split between operating and nonoperating income, with taxes on activities such as the ownership and sale of real estate included in operating income. Other taxes, such as income tax, franchise tax and excise taxes, are recorded as non-operating expenses. Operating and nonoperating expenses are presented under different headings in the Company’s income statement.

The portion of your wages that go directly to the production of the products or services you sell is reported at the top of the report as part of cost of sales (cost of goods sold). The portion of wages and salaries attributable to other activities, such as sales and accounting, is offset by other expenses and classified as indirect costs. A company’s operating margin, also known as the return on sales, is a good indicator of how well the company is being run and the risk it poses. It indicates what proportion of income is available to cover non-operating expenses, such as interest payments, which is why investors and lenders pay particular attention to it.

At the beginning of the income statement, the cost of goods sold is deducted from sales to arrive at the gross profit. The amount remaining after deducting all operating expenses is called operating profit. In short, all expenses that inherently generate revenue and play a supporting role in the operation of the business are operating expenses. It is important to understand that costs incurred for the initial repair of an asset to render it usable or legal fees incurred to acquire the asset are not operating expenses. Similarly, costs incurred in issuing shares or bonds are also capital expenditures and cannot be treated as operating expenses and deducted from the income statement.

These costs are recognised in the income statement as operating expenses as they relate to the performance of the underlying business activity during the reporting period. These costs are an expense because they expire, can be consumed or have no measurable future value.

The objective is to enable users of the financial statements to assess the direct operating activities that only appear at the top of the income statement. It is important for the prospects of the company that the core activities are profitable. Tax losses – or income from tax refunds – are generally not considered business activities, even if companies pay taxes or claim tax credits in each reporting year. The term earnings before interest and taxes is often used as a synonym for operating profit.

This type of income is generally not considered to form part of normal business operations and is therefore recognised in the income statement as non-operating or secondary income. Investments in assets that an entity uses in its main business – such as. B. Plant and equipment – not included in this item.

Difference between operating and capital expenditure

Operating expenses are the costs incurred (forgone) in connection with the entity’s principal business activities during the period reported under the heading of the income statement. Operating expenses can significantly affect a company’s profitability and cash flow. Operating expenses are costs incurred by the company that are not related to the manufacture of products. These expenses include items such as salaries, rent, office supplies, utilities, marketing, insurance and taxes. Operating profit is an accounting ratio that measures the profit generated by a company’s operations after deducting operating expenses such as salaries, depreciation and cost of goods sold (COGS).

Similarly, an evaluation of a company’s past operating margins can help assess whether the significant improvement in sales will be sustainable. Operating margin is widely regarded as one of the most important accounting measures of business efficiency. It measures a company’s operating profit, i.e. total revenue for the period minus operating expenses, divided by net sales.

These costs, such as. B. Personnel and advertising costs are called operating costs. Companies also have non-operating expenses and potentially non-operating revenues, such as B. Potential costs and revenues associated with litigation. It is good accounting practice to distinguish between business and non-business expenses and disclose them separately when reporting business income and expenses. Non-operating expenses, as the name implies, is an accounting term for expenses not related to day-to-day operations.

What are the operating costs?

These types of expenses include monthly payments, such as. B. Interest payments on debt, but may include one-time or unusual expenses. For example, an entity may classify as non-operating expenses costs costs incurred as a result of a reorganisation or restructuring, foreign exchange costs or costs of obsolete inventories. Non-operating costs, on the other hand, are costs incurred by a company that are not related to its core business. The most common types of non-operating expenses are depreciation, interest payments, or other loan costs.

After calculating gross profit, all operating expenses are deducted to arrive at the company’s operating profit or earnings before interest, taxes, depreciation and amortization (EBITDA). All non-operating expenses are then reported in the financial report after the operating result is achieved. To obtain the profit before tax (EBT), the non-operating costs are deducted from the operating profit of the company. Non-operating expenses are recognized at the end of the Company’s income statement.

When you look at a company’s income statement from top to bottom, operating expenses are the first expense item, just below revenue. The company begins the income statement with the top line of sales. Cost of goods sold (COGS) is then deducted from sales to obtain the gross margin.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is included in the operating expenses?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The operating expenses include general and administrative expenses, research and development expenses, and selling, general, and administrative expenses.”}},{“@type”:”Question”,”name”:”What are some examples of operating expenses?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Some examples of operating expenses are rent, utilities, payroll, advertising, and product development.”}},{“@type”:”Question”,”name”:”What is not included in operating expenses?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Interest expense, depreciation, and amortization are not included in operating expenses.”}}]}

Frequently Asked Questions

What is included in the operating expenses?

The operating expenses include general and administrative expenses, research and development expenses, and selling, general, and administrative expenses.

What are some examples of operating expenses?

Some examples of operating expenses are rent, utilities, payroll, advertising, and product development.

What is not included in operating expenses?

Interest expense, depreciation, and amortization are not included in operating expenses.

Maximising Wins: Strategies for Success in Online Slot Gaming

Seasonal Marketing Tactics on Instagram: Customizing Your Ads for Holiday Celebrations and Seasonal Occasions

A Detailed Guide to Purchasing Wholesale Flowers

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Building Your Crypto Knowledge: Must-Read Books and Resources for Enthusiasts

Legal Maneuvers in the Path of Blockchain Evolution

Securing IoT: Blockchain Integration Boosts Safety

Strategies for Personal Finance Growth: Exploring BetterThisWorld Stocks

Cryptographic Currency in Global Transactions: Discovering Affordable Avenues

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home