Straight Line Depreciation Method

When it comes to calculating depreciation for the purpose of tax purposes, an asset’s fair value is used to calculate its value. Depending on the asset, there are different methods of calculating the fair value. Straight Line method is one of the most popular methods of calculating Fair Value for assets.

(This post was cross-posted on http://www.quantacolumn.com/). Straight Line Depreciation Method (SLDM) is a method for calculating the future value of a share, asset or financial instrument based on the actual historical appreciation rate of that asset. SLDM is based on the following assumptions: The annualized compounding rate is the only parameter that matters.

30. October 2020

Accounting Adam Hill

Detailed depreciation is important for companies that use machinery or equipment to manufacture products. It can provide a more accurate picture of gains and losses by allocating the value of these assets over time according to their use. This is useful for producers because production fluctuates according to consumer demand. Most impairment methods use the passage of time to determine the value an asset has lost, for example. For example, a car that is depreciated 20% per year. Unit depreciation reduces the value of plant or machinery according to its use – often in production units.

- You can calculate depreciation expense using either the accelerated depreciation method or the straight-line method over the useful life of the asset.

- The advantage of the accelerated method is that you can depreciate more at the beginning of the useful life of the asset, which allows you to defer the recognition of certain tax costs until a later period.

Double declining balance depreciation is a variant of the accelerated depreciation method. This method reflects higher depreciation amounts in the early years of the useful life and lower depreciation amounts in later years. As a result, revenues and assets will continue to decline in the first few years due to higher depreciation costs.

How does proportionality affect the impairment of assets?

The principal method of permanent depreciation is the straight-line method. The following are two examples of the calculation of depreciation of property, plant and equipment under the unit-of-production method.

Depreciation expense reflects the actual depreciation of these assets and is consistent with revenues and expenses. However, this method cannot be used by all companies or for tax purposes. To calculate unit depreciation, apply the average unit cost rate to the total number of units produced by the machine or equipment each year. This rate would be the ratio of the total cost of the asset less the residual value to the estimated number of units expected to be produced during its useful life.

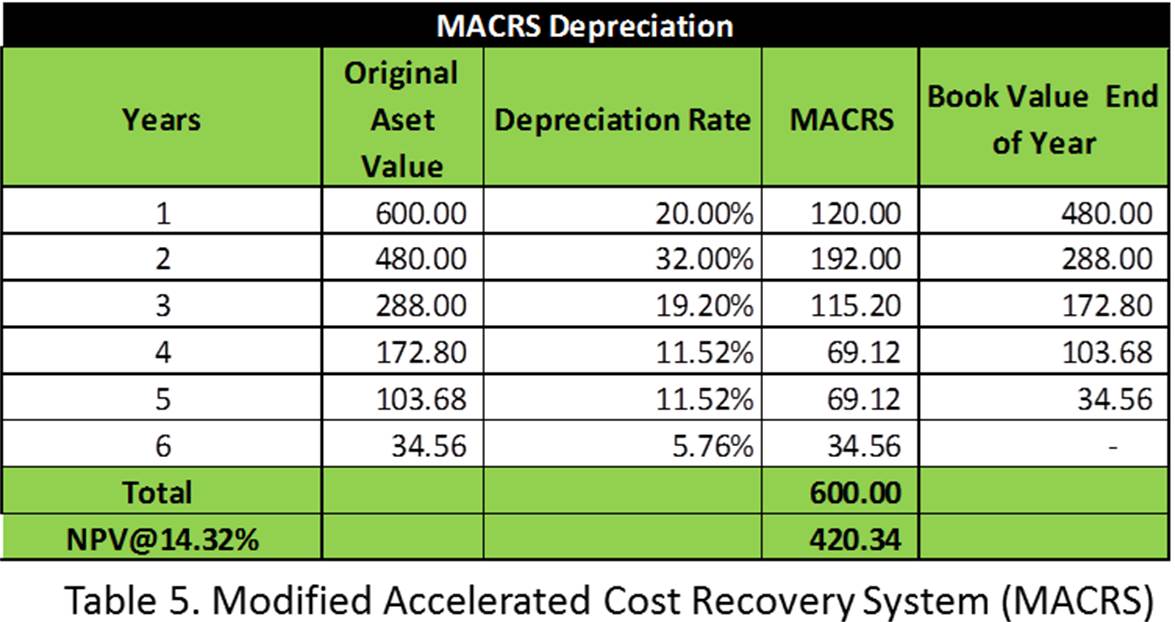

Consequently, depreciation expense fluctuates based on customer demand and the actual depreciation of the asset. The Modified Accelerated Cost Recovery System (MACRS) is the standard method for depreciating assets for tax purposes. After three years, the book value is $200. Depreciation expense is recorded using the straight-line method and management will retire the asset.

Definition of the unit method

You can calculate depreciation expense using either the accelerated depreciation method or the straight-line method over the useful life of the asset. The advantage of the accelerated method is that you can depreciate more at the beginning of the useful life of the asset, which allows you to defer the recognition of certain tax costs until a later period. The advantage of using a constant depreciation rate is that it is easy to calculate. Examples of accelerated depreciation methods are the double declining balance method and the sum of the years method.

However, this is one of four depreciation methods you can use to reflect depreciation in your accounting records. Production units are particularly suitable for manufacturers whose equipment use varies according to customer demand, as they can align revenues and costs. The most common depreciation methods are the straight-line method, the double depreciation method, the unit production method and the annual sum method.

This amount reduces both the cost of the asset and the income for the period. The usual method for calculating depreciation expense is the straight-line method. First, you divide the cost of the asset, less its residual value, by the total number of units expected to be produced by the asset during its estimated useful life. Then multiply this unit cost rate by the total number of units produced in the period.

The first is for the sewing machine and the second is for the tap that was purchased for your plant. The per unit produced depreciation method requires a cost basis, a residual value, an estimated useful life, an estimated total useful life, and actual produced units for sample calculations.

According to the production unit method, the amount of depreciation charged to expenditure evolves in direct proportion to the use of the asset. Therefore, an entity may depreciate more in periods when the assets are used more frequently and less in periods when they are used less frequently.

Whichever method you choose, you should also keep records, as the tax authorities require supporting documents for capital assets. In the event of an inspection, you must provide these documents to prove the cost of the property and the fact that you are the owner. Detailed depreciation can work very well for manufacturing companies that use equipment to manufacture products.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How do you calculate straight line depreciation?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Straight line depreciation is calculated by dividing the cost of an asset by its useful life.”}},{“@type”:”Question”,”name”:”What is the formula for each depreciation method?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Straight-line depreciation: Cost of the asset – salvage value = depreciation expense in the year of purchase. Double-declining balance: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The remaining balance is depreciated over a period of years, with half being deducted each year. Sum-of-the-years’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 10% and adding that amount to the current year’s depreciation expense. Sum-of-the-months’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 12% and adding that amount to the current year’s depreciation expense. Double-declining balance with half-year convention: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The first half of the depreciation is calculated using a half-year convention, with one-half of the annual depreciation being deducted in January and February.”}},{“@type”:”Question”,”name”:”What is SLM method?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” SLM method is a technique for estimating the number of people who are likely to be infected with a disease in a population. What is the difference between SLM and RDM? SLM method is a technique for estimating the number of people who are likely to be infected with a disease in a population. RDM method is an estimation of the number of people who will be diagnosed with a disease in a population.”}}]}

Frequently Asked Questions

How do you calculate straight line depreciation?

Straight line depreciation is calculated by dividing the cost of an asset by its useful life.

What is the formula for each depreciation method?

Straight-line depreciation: Cost of the asset – salvage value = depreciation expense in the year of purchase. Double-declining balance: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The remaining balance is depreciated over a period of years, with half being deducted each year. Sum-of-the-years’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 10% and adding that amount to the current year’s depreciation expense. Sum-of-the-months’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 12% and adding that amount to the current year’s depreciation expense. Double-declining balance with half-year convention: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The first half of the depreciation is calculated using a half-year convention, with one-half of the annual depreciation being deducted in January and February.

What is SLM method?

SLM method is a technique for estimating the number of people who are likely to be infected with a disease in a population. What is the difference between SLM and RDM? SLM method is a technique for estimating the number of people who are likely to be infected with a disease in a population. RDM method is an estimation of the number of people who will be diagnosed with a disease in a population.

Step-By-Step Guide to Filing a Personal Injury Claim

Forming a Healthy Relationship with Money – Tips to Improve your Money Mindset

The Ultimate Guide to the Best Online Casinos in Japan

Unwinding the Secrets of Cryoglobulinemia: A Complete Aide

4 Benefits of Document Digitizing Services for Businesses

10 Biggest Cryptocurrency Exchanges of 2024

How to Identify and Choose Trusted Online Casinos in Malaysia

Discovering Perfect Outfit Combinations: Celana Coklat Cocok Dengan Baju Warna Apa

Converting 50 Riyal Berapa Rupiah: Currency Exchange Rate Explained

Duniaklub: Top Slot Games & Exclusive Bonuses

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance3 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home