Selling expense

If you have ever tried to sell your home, you will have probably been asked one of the most common questions people ask you. I am sure it’s something along the lines of, “so, what was it like to sell your house?”, “how much did you get for it?”, “how many offers did you get?”, “how many people came to view it?”. The question is usually asked because it is a statement of fact and everybody wants to know the answer.

This is a blog that discusses various topics about selling expenses. Some of them are: how to invest in selling expenses, how to sell your selling expense at the right time, how to get good profit from selling expenses, etc.

Home accounting Distribution costs

7. October 2020

Accounting Adam Hill

However, you should not underestimate the importance of these management decisions to the performance of the company for investors. The way management aggregates and analyzes its expenses implicitly determines how it sees and understands the business. Management makes decisions based on the data it has, and these management accounting decisions give context to the data.

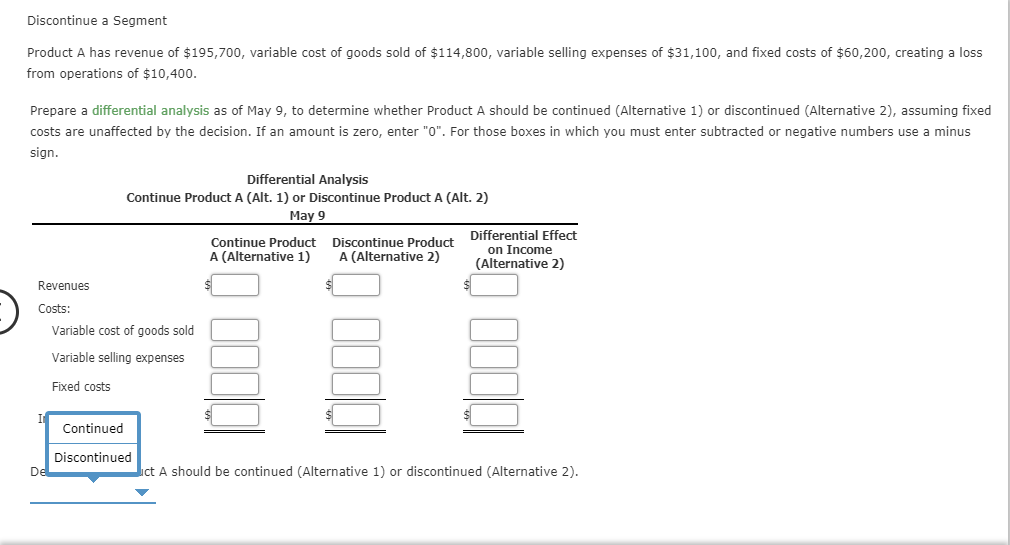

Calculation of the cost of goods sold

Managing this part of the income statement is an essential part of running a successful business. General and administrative expenses are generally costs that a company incurs anyway, whether it produces or sells something. This type of expense is generally included in cost of goods sold (COGS) in the income statement and is combined with selling expenses in a single line item for selling, general and administrative expenses. Information on these types of costs is particularly useful for calculating the company’s fixed costs.

This part of the budget contains the expected operating costs of the holding, excluding direct production costs. The company’s production costs are classified as cost of goods sold and have their own category in the projected income statement. Selling, general and administrative expenses are usually a significant item on a company’s income statement. It includes almost all expenses of the company that are not directly related to the production of products. If a company wants to grow, reduce its costs or simply maintain the level it has reached, managers must pay particular attention to this indicator and all its components.

Selling expenses are generally included in operating expenses in the income statement, which are less than the cost of sales. Gross profit is the direct profit remaining after deducting cost of goods sold or cost of sales. It is used to calculate the gross profit margin and is the first profit figure that appears on the company’s income statement.

Selling and administrative expenses also include non-cash expenses such as depreciation and amortization. As with fixed costs, we have little control over recurring costs, but while fixed costs typically recur at the same time each month, recurring costs are what I call expected unexpected costs. It seems like an oxymoron to have an expected surprise, but I’m sure you were all there.

As you may have guessed, commercial and administrative costs vary quite a bit. They include both highly variable costs, such as marketing, and essentially fixed costs, such as rent.

In general, all costs which are not related to the production or sales process and which are not part of research and development are classified as general and administrative expenses. Therefore, general and administrative expenses are not related to the cost of sales and do not represent stocks. General and administrative expenses are also generally constant, since they remain constant regardless of the level of sales.

In order to create a budget, a company must first decide which unit of time it wants to use. A budget calculated on a monthly basis generally provides a good level of detail, while some companies prefer a higher budget on a quarterly basis. Since some operating expenses depend on sales volume, the expected number of units to be sold becomes the starting point for the budget.

The income statement is one of the most important financial statements of a company. It shows the profits and losses over a given period. Distribution costs, often called cost of goods sold, refer to the costs and purchases required to create the products or services for which consumers pay your small business. The difference between the sales revenue and the cost of sales determines the gross profit, from which overhead costs are subtracted to calculate the net profit. Most companies calculate operating expenses on a monthly basis, but it can also be done on a weekly or quarterly basis. If the premises rented are used for the production of goods, the rent is part of the value of the goods produced.

Under the revenue method, a fixed percentage is applied to the total revenue for the period. For example, on the basis of past experience, an entity may assume that 3 % of net sales are not recoverable. If total net revenues for the period are $100,000, the entity establishes an allowance for doubtful accounts of $3,000 and simultaneously records a charge for doubtful accounts of $3,000. If net sales in the next reporting period are $80,000, an additional $2,400 is recorded in the second period as an allowance for doubtful accounts and $2,400 is recorded as an expense for doubtful accounts. The cumulative balance of the allowance for doubtful accounts after these two periods is $5,400.

Companies look at cost of sales versus other administrative costs to determine if the company is properly allocating its resources to personnel and marketing. In the company’s general income statement, these costs are included in revenue, cost of sales and other expenses, such as interest and depreciation. The sales and administration budget is part of the company’s pro forma or budgeted income statement.

Bad debts are generally classified as selling, general and administrative expenses and are recognized in the income statement. Recognition of doubtful debts leads to a reduction of the balance sheet receivable, although companies retain the right to recover debts if circumstances change. An efficient company maximizes production and sales in relation to operating expenses, which include selling and administrative expenses. If production exceeds sales force revenue, slow down production or make changes to increase revenue and reduce overhead until the company finds an operational break-even point. In the income statement, administrative expenses are presented under cost of sales and may be combined with other expenses, such as e. overheads or distribution costs.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is considered a selling expense?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A selling expense is an expense incurred in the process of selling a product or service.”}},{“@type”:”Question”,”name”:”How do you find the selling expense?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The selling expense is the cost of goods sold.”}},{“@type”:”Question”,”name”:”What is the difference between selling expenses and general or administrative expenses?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Selling expenses are costs incurred in the process of selling goods or services. General and administrative expenses are costs incurred in the process of running a business.”}}]}

Frequently Asked Questions

What is considered a selling expense?

A selling expense is an expense incurred in the process of selling a product or service.

How do you find the selling expense?

The selling expense is the cost of goods sold.

What is the difference between selling expenses and general or administrative expenses?

Selling expenses are costs incurred in the process of selling goods or services. General and administrative expenses are costs incurred in the process of running a business.

How to Choose the Right CBD Vape Pen for Your Needs: A Purchaser’s Guide

How To Choose a Wedding Ring to Match a Profession

Maximising Wins: Strategies for Success in Online Slot Gaming

Seasonal Marketing Tactics on Instagram: Customizing Your Ads for Holiday Celebrations and Seasonal Occasions

A Detailed Guide to Purchasing Wholesale Flowers

Strategies for Personal Finance Growth: Exploring BetterThisWorld Stocks

Engage, Learn and Impact: The Btwradiovent Event by Betterthisworld Explored

Explore the Strategic Advantages of Betterthiscosmos Posts

Smart Spending, Stylish Living: Finding Discounts on Luxury Brands

Mastering YY4D Login: A Step-by-Step Guide to Secure User Experience

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home