PVIF Calculator

Before you start investing, you should figure out how much money you have to invest, and how much you want to set aside for retirement. Once you know those two numbers, you can look at certain investment options to see if they fit your budget.

This is an important calculator for all new buyers of solar panels. The calculation is really simple and takes only a few minutes. I will walk you through the process and show you the results of the calculations.

PVIF calculator for internal accounting

18. September 2020

Accounting Adam Hill

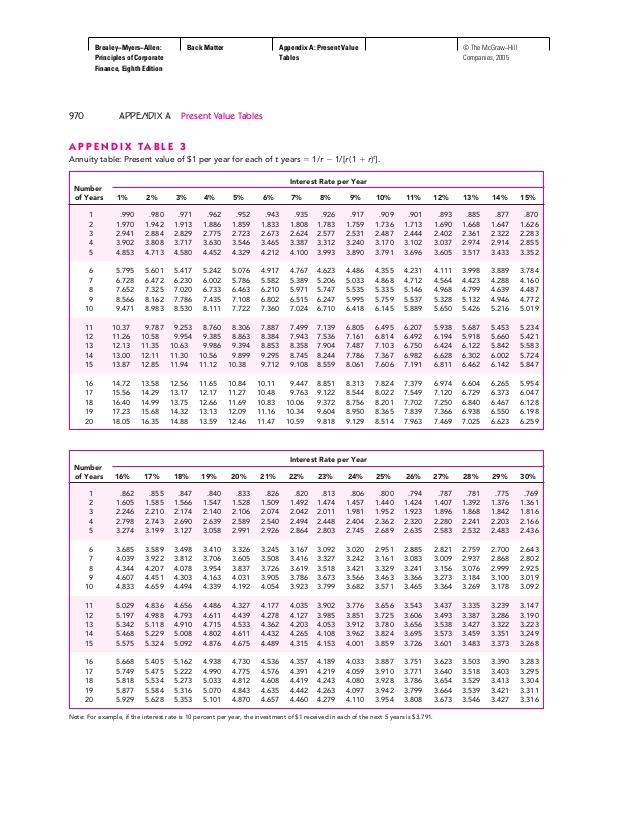

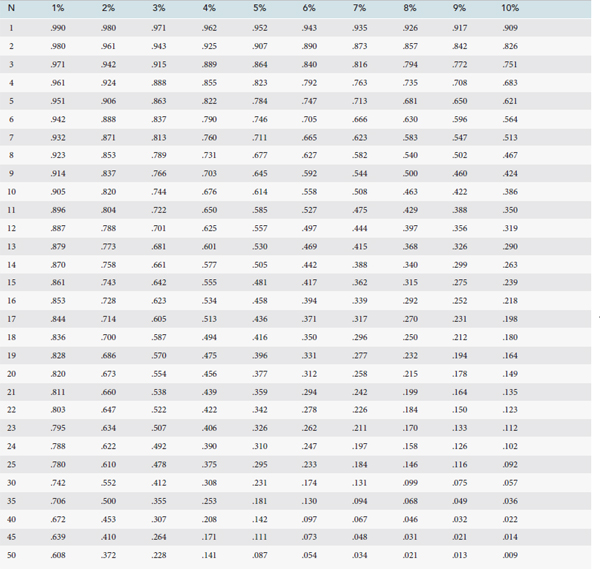

Behind every spreadsheet, calculator and software program are the mathematical formulas needed to calculate present value, interest rate, number of periods and amount of future value. First, we’ll show you some examples of how to use the NPV formula in addition to the PV tables. If you do not have access to an electronic financial calculator or software, a simple way to calculate present value is to use present value tables (PV).

A dollar today is worth more than a dollar tomorrow, because a dollar can be invested and earn interest every day, so by tomorrow a total of more than a dollar can be accumulated. By giving the borrower access to money, the lender sacrifices the exchange value of that money and is compensated in the form of interest. The original amount of money borrowed (present value) is less than the total amount of money paid to the lender.

This table is used in the same way as the other time value of money tables. The present value interest is based on the central financial concept of the time value of money.

This table generally provides the present value factors for different periods and combinations of discount rates. Although using present value tables is a simple way to determine the present value factor, it has a limitation. Interest is the extra amount of money received between the beginning and the end of a period.

It has a useful life of 5 years and a residual value of $5,000. Annual operating costs will be $20,000. This machine is expected to generate annual net income of $45,000. The company’s required rate of return is 15% (the same as the previous year). Determine the payback period for this investment using Table 8.1 Calculation of payback period for Jackson quality copies.

Since the factors in the PV table are rounded to 1 to 3 decimal places, the answer ($85.70) differs slightly from the amount calculated using the PV formula ($85.73). The present value of the amount of money that will be received in the future is determined by discounting the future value at the interest rate that the money could earn during that period. Cash flows consist of discounting each cash flow to present value using a present value ratio and an appropriate number of capitalization periods, and combining these values. The process of estimating the current amount of money at some point in the future is called capitalization (how much will $100 be worth today in five years?). The reverse operation, estimating the present value of a future sum of money, is called discounting (how much is the $100 you will receive in five years worth today).

Interest represents the time value of money and can be thought of as the rent that the borrower charges the lender for the use of the money. For example, when a person takes out a bank loan, he or she must pay interest.

The initial investment to purchase the building is $420,000, with an additional $50,000 needed for working capital. Since this company will continue to operate for many years, the working capital will not be repaid in the near future. Tower wants to remodel the store by the end of year 3 for $100,000. The annual net cash flow from operating activities (cash receipts less cash disbursements) is expected to be as follows

In fact, the money can be put in a bank account or another (safe) investment that will earn interest in the future. In economics and finance, present value (NPV), also known as discounted value, is the value of the expected income stream at the valuation date. The time value can be described using a simplified formulation: A dollar today is worth more than a dollar tomorrow. More value here means higher value.

For example, interest that accrues annually is recorded once a year and the accrual period is one year. Interest is calculated quarterly and accrues four times per year with an accrual period of three months. The compounding period can be any period, but some common periods are annual, semiannual, quarterly, monthly, daily and even continuous.

If one has a choice between $100 today and $100 a year from now, and if the real interest rate in that year is positive, a rational person would ceteris paribus choose $100 today. Economists call this time preference. The time preference can be obtained by auctioning a risk-free security, for example. such as a U.S. Treasury bond, can be measured. If a $100 note with a zero coupon that matures in one year is sold now for $80, $80 is the cash value of the note, which will be worth $100 in one year.

Both present value and future value calculations are used to determine the value of loans, mortgages, annuities, sinking funds, perpetual contracts, bonds, etc. These calculations are used to make comparisons between cash flows that do not occur at the same time, as the timing must be consistent to make comparisons between values. The project with the highest current value, i.e. the project with the highest value today, should be selected. The present value table or PV table shows different time periods in the first row and different discount rates in the first column. The table shows the present value coefficients for a given discount rate and time.

The periods can be expressed in weeks, months or years and the discount rates are usually between 0 and 20% with intervals of 0.25% or 0.50%. The present value of an annuity is the present value of future payments of that annuity, taking into account a specified rate of return or discount. Wood Products Company wants to buy a computerized wood lathe for $100,000.

- The Discounted Interest Rate Factor (DIRF) is a formula used to estimate the present value of a sum of money to be received at a future date.

- The concepts of NPV and NPV factors play an important role in investment appraisal and capital budgeting.

PV tables cannot provide the same accuracy as financial calculators or computer programs because the factors used in the tables are rounded to fewer decimal places. Moreover, they usually have a limited number of interest rate and maturity options. Nevertheless, tables with the given value remain popular in academia because they can be easily incorporated into a textbook. Because of its widespread use, we will use cash value tables to solve our examples. The first column (n) indicates the number of repeated identical payments (or periods) in the year.

Table NPV 1 shows the NPV rates used for different combinations of interest rates and time periods. The discount rate chosen from this table is then multiplied by the amount of money that will be received in the future to obtain the present value. The interest rate chosen in the table may be based on the current amount the investor receives from other investments, the cost of capital of the company, or some other parameter. The discount rate or interest rate, on the other hand, refers to the rate of interest or return that an investment may yield over a period of time.

Become a PRO or PRO Plus member and get lifetime access to our premium content

The Discounted Interest Rate Factor (DIRF) is a formula used to estimate the present value of a sum of money to be received at a future date. PVIFs are often tabulated with values for different time periods and interest rate combinations. The concepts of NPV and NPV factors play an important role in investment appraisal and capital budgeting.

Present value formula, tables and calculators

Or else: When someone puts money in a bank, he or she receives interest on that money. In this case, the bank is the borrower of the funds and must charge interest to the account holder. The compounding period is the time that must elapse before interest is accrued or added to the total amount.

The cash value ratio is based on the concept of the time value of money, which states that a dollar received today is worth more than a dollar received in the future. The reason is that the value of money increases over time as long as the interest rate is above zero. Thus, when the future value is multiplied by these factors, the future value is discounted to the present value.

The discounted annuity valuation factor in percent (PVIFA) is helpful in deciding whether to take a lump sum payment now or accept an annuity payment in future periods. Using the estimated returns, you can compare the cost of annuities to the cost of capital. The present value ratio, also known as the percentage present value ratio (PVIF), is a ratio used to calculate the present value of money that will be received at a future date. In other words, this factor helps us determine whether money received now is worth more or less than when it is received later. For simplicity, the present value factor is often presented in tabular form.

Calculation of the present value (PV) of a unit amount

This means that today’s amount of money is worth more than the same amount will be worth in the future, since money has the potential to increase in value over time. To the extent that money can earn interest, the faster it is received, the higher the value of a sum of money. Analysis of net present value, internal rate of return and payback period; ethical issues. Tower CD Stores is looking to open a store in Houston.

In the table, time can be specified in weeks, months or years. The discount rates generally range from 0 to 20% with a margin of 0.25% or 0.50% or 1%. What is the definition of a cash value table? In Table PV, the first column shows the different discount rates and the first row shows the different time periods. The purpose of this table is to present the value coefficients for different periods and different discount rates.

Balance sheet ratios

It is so called because it is the discount rate by which the future value of money is discounted to its present value. Present value effect factors are often used in annuity analysis.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How do you calculate PVIF?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” PVIF is calculated by taking the present value of a future cash flow and dividing it by the discount rate.”}},{“@type”:”Question”,”name”:”What is the PVIF for 15% of 5th year?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The PVIF for 15% of 5th year is 0.15.”}},{“@type”:”Question”,”name”:”How is Pvifa calculated online?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Pvifa is calculated online by multiplying the number of hours in a day by the hourly wage.”}}]}

Frequently Asked Questions

How do you calculate PVIF?

PVIF is calculated by taking the present value of a future cash flow and dividing it by the discount rate.

What is the PVIF for 15% of 5th year?

The PVIF for 15% of 5th year is 0.15.

How is Pvifa calculated online?

Pvifa is calculated online by multiplying the number of hours in a day by the hourly wage.

Cybersecurity Trends to Watch in 2024

Uncovering Dundee’s Roots As A Scottish Tech Powerhouse

From Panic to Peace: Utilizing Therapy & Anxiety Coping Mechanisms

Mastering Product Descriptions with ChatGPT: A Comprehensive Guide

Crypto Education for Beginners: A Comprehensive Overview of Cryptocurrency

Mastering YY4D Login: A Step-by-Step Guide to Secure User Experience

Exploring Btwradiovent Event by Betterthisworld: BetterThisWorld’s Revolutionary Event on Digital Broadcasting and Social Reform

The 4 Tips To Help You Move To A Tropical Country

Mastering Jeboltogel Login Alternatif: A Comprehensive Guide for Seamless Gaming Experience

Gaming Evolution: The Transition From Real-World to Online Casinos

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home