Efficiency variance

The effectiveness of a company’s financial management is crucial to its long-term success, as this dictates its ability to maintain steady returns and take advantage of opportunities in the market. While there are a number of ways to gauge the effectiveness of a company’s financial management, the most accurate gauge is through variance ratios.

This is the first in a series of articles on efficiency variability. As the name suggests, efficiency variability is the variation in the efficiency of decisions. It is often expressed as the Sharpe ratio and the Jensen, Sortino and Treynor (JST) ratio. These metrics relate to the expected excess return on a portfolio given its level of risk.

Home » Bookkeeping » Efficiency variance

Aug 17, 2020

Bookkeeping by Adam Hill

About Labor Variances

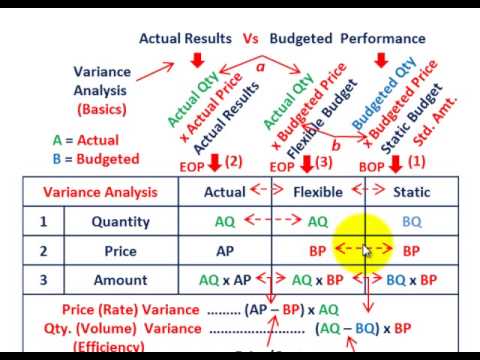

The labor efficiency variance focuses on the quantity of labor hours used in production. It is defined as the difference between the actual number of direct labor hours worked and budgeted direct labor hours that should have been worked based on the standards. This information gives the management a way to monitor and control production costs. Next, we calculate and analyze variable manufacturing overhead cost variances. These include all the expenses you pay outside of labor costs — things like building costs, property taxes, and utilities — and they can be calculated either monthly or annually, depending on the needs of your business.

The units produced are the equivalent units of production for the labor cost being analyzed. Labor efficiency variance is also known as labor time variance and labor usage variance. Labor price variance equals the standard hourly rate you pay direct labor employees minus the actual hourly rate you pay them, times the actual hours they work during a certain period. For example, assume your small business budgets a standard labor rate of $20 per hour and pays your employees an actual rate of $18 per hour.

It also includes other benefits such as worker’s compensation and unemployment insurance, health insurance and contributions to pension or retirement plans. The efficiency variance is the difference between the actual unit usage of something and the expected amount of it. The expected amount is usually the standard quantity of direct materials, direct labor, machine usage time, and so forth that is assigned to a product. For example, an efficiency variance can be calculated for the number of hours required to complete an audit versus the budgeted amount. Labor efficiency variance is calculated by comparing the actual hours worked with standard hours allowed, both at the standard labor rate.

Suppose XYZ Widgets employs a direct labor workforce of 10 people, who work 40 hours per week, and they earn an average of $18 per hour. Total wages are equal to 40 hours multiplied by $18 and then multiplied by 10. Additional payroll taxes and benefits total $1,800, which gives a total direct labor weekly payroll expenditure of $9,000. Ten workers normally work 400 hours in a week, so the standard or average cost of one hour of direct labor equals $9,000 divided by 400, or $22.50. Recall from Figure 10.1 “Standard Costs at Jerry’s Ice Cream” that the standard rate for Jerry’s is $13 per direct labor hour and the standard direct labor hours is 0.10 per unit.

Companies typically try to lock in a standard price per unit for raw materials, but sometimes suppliers raise prices due to inflation, a shortage or increasing business costs. If there wasn’t enough supply available of the necessary raw materials, the company purchasing agent may have been forced to buy a more expensive alternative.

To figure it out, just divide your total annual overhead costs by the number of employees at your business. The cost of labor is the sum of each employee’s gross wages, in addition to all other expenses paid per employee. Other expenses include payroll taxes, benefits, insurance, paid time off, meals, and equipment or supplies.

If the company bought a smaller quantity of raw materials, they may not have qualified for favorable bulk pricing rates. To calculate the labor burden, add each employee’s wages, payroll taxes, and benefits to an employer’s annual overhead costs (building costs, property taxes, utilities, equipment, insurance, and benefits). Standard costs are used to establish the flexible budget for direct labor. The flexible budget is compared to actual costs, and the difference is shown in the form of two variances. The labor rate variance focuses on the wages paid for labor and is defined as the difference between actual costs for direct labor and budgeted costs based on the standards.

Other factory floor employees are considered indirect labor because their jobs are not immediately tied to making the product. Equipment maintenance technicians and security guards fall into this category. The difference is crucial because only direct labor is counted as part of the cost of manufacturing a good. Direct labor includes wages plus employer-paid payroll taxes like Social Security and Medicare tax.

Direct Labor Efficiency Variance Calculation

Your labor price variance would be $20 minus $18, times 400, which equals a favorable $800. Fixed labor cost remains the same regardless of the company’s production output.

The standard hours allowed figure is determined by multiplying direct labor hours established or predetermined to produce a single unit by the number of units produced. For example, if standard time to produce one unit of a product is 2 hours and 10 units of product have been manufactured during the period than the standard time allows would be 20 hours (2 × 10).

This will help determine how much an employee costs their employer per hour. It is important to have a consistent employee timesheetsoftware or app for long term labor cost success. Once the total overhead is added together, divide it by the number of employees, and add that figure to the employee’s annual labor cost. The material price variance calculation tells managers how much money was spent or saved, but it doesn’t tell them why the variance happened. One common reason for unfavorable price variances is a price change from the vendor.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How do you calculate material efficiency variance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Material efficiency variance is calculated by taking the difference between the actual material cost and the budgeted material cost.”}},{“@type”:”Question”,”name”:”What is labor efficiency variance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Labor efficiency variance is the difference between the actual labor hours used and the standard labor hours used.”}},{“@type”:”Question”,”name”:”Is efficiency variance same as volume variance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” No, efficiency variance is the difference between the total revenue and total cost. Volume variance is the difference between the total revenue and total volume.”}}]}

Frequently Asked Questions

How do you calculate material efficiency variance?

Material efficiency variance is calculated by taking the difference between the actual material cost and the budgeted material cost.

What is labor efficiency variance?

Labor efficiency variance is the difference between the actual labor hours used and the standard labor hours used.

Is efficiency variance same as volume variance?

No, efficiency variance is the difference between the total revenue and total cost. Volume variance is the difference between the total revenue and total volume.

Immersion is the Ultimate Goal of Gaming Platforms

Boosting Solar Business Efficiency and Customer Satisfaction with FSM

Possible Risks of Shrooms Online Purchase

Silk Bonnets and LED Panels for Skin Health and Sleep Quality

From Pixels to Payouts: Exploring the Art and Technology of Online Slot Design

How Barcode Technology Improves Emergency Room Operations

Still Thinking About Rome? How to Immerse Yourself in this Idealised Period of History

BetterThisWorld com: Unveiling New Perspectives

Paito Cambodia Harian: Your Ultimate Guide to Daily Trends

The Benefits of a D3K2 Supplement: Unlocking the Power of Vitamins D3 and K2

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home