Depreciation Methods: Check Formula, Factors & Types

Depreciation Methods: Check Formula, Factors & Types

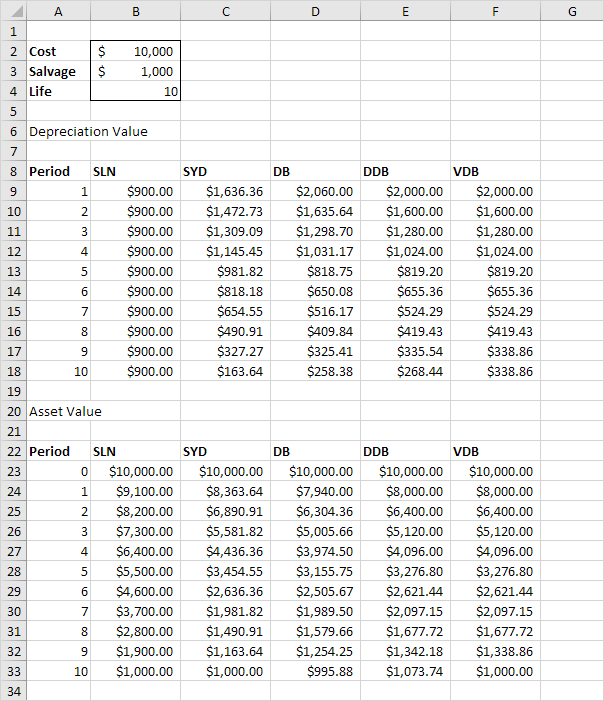

As the topic says, this post is going to be about depreciation methods. They can be classified into 3 types: The first type is the straight-line method. It makes use of the declining balance method. This method assumes that an asset is fully depreciated over the period of the lease or loan. After which, the asset is reassessed at the present value, keeping in mind that the new value is higher than the original cost. The second method is the declining balance method. This type of depreciation is used to calculate depreciation of plant and machinery. It assumes that an asset is depreciated over the period of the lease or loan using the straight-line method. The third method is the remaining useful life method. This

The method of depreciating assets is the same for all assets. For instance, both an investment of Rs.5,000 and Rs.6,000 in a hotel are depreciated at the rate of 12% per annum, which means every year, 2/12th of the original investment is deducted. This is called the ‘indexation method’. The second method is called the ‘cost segregation method’. The ‘indexation method’ is a little complex in that depreciation is charged at different rates on different assets.

Accounting Home Accounting Depreciation Methods : Formula, factors and types of tests

24. August 2020

Accounting Adam Hill

For our calculations, we assume that the client in the sample falls into the 30% tax bracket. This model is designed to assist accountants and other financial professionals in calculating the tax depreciation of assets subject to the Modified Accelerated Cost Recovery System (MACRS) rules. The model calculates both depreciation over 5 years and depreciation over 7 years.

Property class tableMACRS GDS

Eligible solar photovoltaic systems are eligible for five years. For systems using the investment tax credit (ITC), the owner must reduce the project’s tax base by half the value of the 30% ITC.

The Modified Accelerated Cost Recovery System (MACRS) is the tax depreciation system currently used in the United States. Under this system, the capitalized cost (basis) of property, plant and equipment is depreciated over a specified useful life through annual depreciation charges. The Internal Revenue Service (IRS) publishes detailed mortality tables by asset class. The depreciation deduction is calculated according to one of two methods (degressive, transition to linear or straight-line), at the choice of the taxpayer, subject to certain restrictions.

Accounting tools

In 1981, Congress again amended the depreciation system to provide generally for a shorter useful life for cost recovery purposes. Under the Accelerated Cost Recovery System (ACRS), large groups of assets were imputed according to the old ACRS terms (which the IRS has since modified). Taxpayers were only allowed to depreciate on a declining balance basis, by conversion to straight-line depreciation, or on a straight-line basis. In response to the 2008 economic downturn, Congress took steps to further stimulate capital investment by accelerating the economy-wide depreciation schedule.

The Tax Relief, Unemployment Insurance Renewal and Job Creation Act of 2010 allowed businesses to claim a 100% depreciation deduction for qualifying capital assets purchased and placed in service prior to December 31, 2011. Congress in early 2013 included in the so-called fiscal cliff deal an extension of bonus depreciation of 50 percent, which was set to expire at the end of 2013. Under the 50% bonus amortization for the first year, companies may elect to amortize 50% of the basis with the remaining 50% being amortized over the normal MACRS amortization period. MACRS depreciation is an important tool for companies to recover certain capital costs over the useful life of an asset.

MACRS

Allowing companies to deduct the depreciation base over five years reduces the tax burden and accelerates the return on investment in solar installations. This has greatly stimulated the development of solar energy and other energy industries. Properties leased27.5 yearsRent contracts acquired after December 31, 2015. December 1986 were executed.

Tax deductions for depreciation have been allowed in the United States since the introduction of the income tax. Prior to 1971, under the old Bulletin F, these deductions could be calculated in different ways over different periods of time. In 1971, Congress enacted the Asset Depreciation Range (ADR) system to simplify calculations and provide consistency. Under ADR, the IRS determines the useful lives of asset classes based on the type or use of the asset. These classes include general classes (e.g. office equipment) and industrial classes (e.g. equipment used in the manufacture of rubber products). Taxpayers can use one of several methods to depreciate assets, including the straight-line method, the declining balance method, and the sum-of-years method.

We will first examine the underlying principles of this approach and then move on to practical application. The Modified Accelerated Cost Recovery System (MACRS) is a depreciation system used for tax purposes in the United States. MACRS amortizes the capitalized cost of an asset over a period of time through annual deductions.

The holding company and its subsidiaries have filed a consolidated tax return. Brookshire used a modified accelerated cost recovery system (MACRS) to recover the value of the property, plant and equipment it used in its operations. In 1991, Brookshire began building gas stations on the site of its grocery stores. It identified the station as non-residential property and recorded depreciation on a straight-line basis for 3.5 years and 39 years after the change in recovery period.

Depreciation is the loss of value that occurs over time when a purchased asset is used in a particular application. As an entrepreneur, you are entitled to deduct this depreciation from your taxable income if it is used for your business. If you have a profitable business and can demonstrate that the solar energy you produce is for business use (as opposed to personal use), this can have a significant impact on reducing your net profit.In this post, I will be discussing the main factors that can impact depreciating assets and how they work. Depreciation is one of the most important concepts that investors and entrepreneurs must understand when assessing the profitability of their business. It is a process that takes time and is an important part of projecting the future financial performance of a company.. Read more about declining balance depreciation formula and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How do you calculate depreciation factor?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The depreciation factor is the ratio of the cost of an asset to its salvage value.”}},{“@type”:”Question”,”name”:”What is the formula for each depreciation method?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Straight-line depreciation: Cost of the asset – salvage value = depreciation expense in the year of purchase. Double-declining balance: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The remaining balance is depreciated over a period of years, with half being deducted each year. Sum-of-the-years’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 10% and adding that amount to the current year’s depreciation expense. Sum-of-the-months’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 12% and adding that amount to the current year’s depreciation expense. Double-declining balance with half-year convention: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The first half of the depreciation is calculated using a half-year convention, with one-half of the annual depreciation being deducted in January and February.”}},{“@type”:”Question”,”name”:”What are the 3 factors that determine how much depreciation you can deduct?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The 3 factors that determine how much depreciation you can deduct are the cost of the property, its useful life, and your tax bracket.”}}]}

Frequently Asked Questions

How do you calculate depreciation factor?

The depreciation factor is the ratio of the cost of an asset to its salvage value.

What is the formula for each depreciation method?

Straight-line depreciation: Cost of the asset – salvage value = depreciation expense in the year of purchase. Double-declining balance: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The remaining balance is depreciated over a period of years, with half being deducted each year. Sum-of-the-years’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 10% and adding that amount to the current year’s depreciation expense. Sum-of-the-months’ digits: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The depreciation expense in each subsequent year is calculated by multiplying the previous year’s depreciation expense by 12% and adding that amount to the current year’s depreciation expense. Double-declining balance with half-year convention: Depreciation expense in the first year is equal to cost of the asset minus its salvage value. The first half of the depreciation is calculated using a half-year convention, with one-half of the annual depreciation being deducted in January and February.

What are the 3 factors that determine how much depreciation you can deduct?

The 3 factors that determine how much depreciation you can deduct are the cost of the property, its useful life, and your tax bracket.

Maximising Wins: Strategies for Success in Online Slot Gaming

Seasonal Marketing Tactics on Instagram: Customizing Your Ads for Holiday Celebrations and Seasonal Occasions

A Detailed Guide to Purchasing Wholesale Flowers

A Guide to Fury vs Usyk

Precious Metals Investments for Beginners: Why You Should Do It

Building Your Crypto Knowledge: Must-Read Books and Resources for Enthusiasts

Legal Maneuvers in the Path of Blockchain Evolution

Securing IoT: Blockchain Integration Boosts Safety

Strategies for Personal Finance Growth: Exploring BetterThisWorld Stocks

Cryptographic Currency in Global Transactions: Discovering Affordable Avenues

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home