Cost of Goods Sold Journal Entry

To start, you will need to take a look at this post from https://profitwithsales.wordpress.com/2015/01/12/how-to-create-your-cost-of-goods-sold-journal-entry/

This blog is a journal where I will post my thoughts and ideas on various topics. I will not be posting about my personal life unless it has some relevance to the topic I am discussing. You can expect to see articles about software development, finance, personal finance, mathematics, and other topics that interest me.

Home » Bookkeeping » Cost of Goods Sold Journal Entry

Aug 14, 2020

Bookkeeping by Adam Hill

How to Take a Reserve Against Your Inventory

On the other hand, failure to properly inventory a supply chain with necessary MRO items can result in production shut-downs and slow-downs, diminished product availability, and ultimately customer attrition. Inventory items at any of the three production stages can change in value. Changes in value can occur for a number of reasons including depreciation, deterioration, obsolescence, change in customer taste, increased demand, decreased market supply, and so on. An accurate inventory accounting system will keep track of these changes to inventory goods at all three production stages and adjust company asset values and the costs associated with the inventory accordingly. As such, the purpose of each seems to be that of maintaining a high level of customer service or part of an attempt to minimize overall costs.

Buffer inventory is the inventory kept or purchased for the purpose of meeting future uncertainties. Also known as safety stock, it is the amount of inventory besides the current inventory requirement. The benefit is smooth business flow and customer satisfaction and disadvantage is the carrying cost of inventory. Raw material as buffer stock is kept for achieving nonstop production and finished goods for delivering any size, any type of order by the customer. Oftentimes, firms will purchase and hold inventory that is in excess of their current need in anticipation of a possible future event.

What is the double entry for inventory?

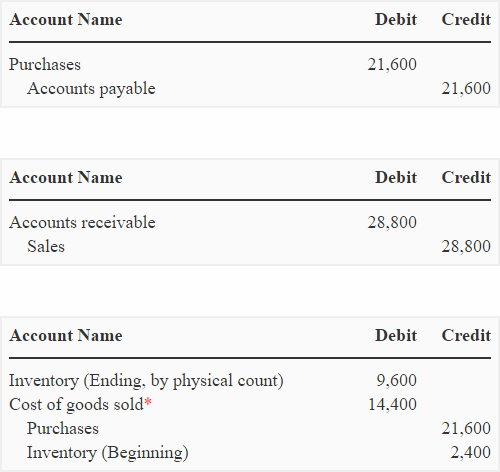

Create a journal entry When adding a COGS journal entry, you will debit your COGS Expense account and credit your Purchases and Inventory accounts. Purchases are decreased by credits and inventory is increased by credits. You will credit your Purchases account to record the amount spent on the materials.

This process is sometimes called “smoothing” because it smoothes the peaks and valleys in demand, allowing the firm to maintain a constant level of output and a stable workforce. These goods are maintained on hand at or near a business’s location so that the firm may meet demand and fulfill its reason for existence. If the firm is a retail establishment, a customer may look elsewhere to have his or her needs satisfied if the firm does not have the required item in stock when the customer arrives.

Thus, they mistakenly assume items that have been stolen have been sold and include their cost in cost of goods sold. Raw materials of all types are initially recorded into an inventory asset account with a debit to the raw materials inventory account and a credit to the accounts payable account. The cost of raw materials on hand as of the balance sheet date appears in the balance sheet as a current asset.

Three general types of inventory control systems include continuous review systems, periodic review systems, and just-in-time inventory control. Raw materials may sometimes be declared obsolete, possibly because they are no longer used in company products, or because they have degraded while in storage, and so can no longer be used. If so, they are typically charged directly to the cost of goods sold, with an offsetting credit to the raw materials inventory account. Consolidating MRO suppliers, when possible, also makes good fiscal sense, as shaving even just a few percentage points from an MRO budget can radically improve a company’s bottom line.

Inventory is either the finished goods stored and offered for sale by a business or the raw materials used by a company to produce finished products. An inventory control system is a process businesses use to manage inventory.

If you buy $100 in raw materials to manufacture your product, you would debit your raw materials inventory and credit your accounts payable. Once that $100 of raw material is moved to the work-in-process phase, the work-in-process inventory account is debited and the raw material inventory account is credited.

Although periodic inventory procedure reduces record-keeping, it also reduces control over inventory items. Firms assume any items not included in the physical count of inventory at the end of the period have been sold.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is the journal entry for cost of goods sold?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Cost of goods sold is the cost of the goods sold during a specific period. The journal entry for cost of goods sold would be as follows: Cost of Goods Sold .. $1,000 Cash . $1,000 Accounts Receivable . $1,000 Inventory . $1,000 The journal entry for cost of goods sold would be as follows: Cost of Goods Sold . $1,000″}},{“@type”:”Question”,”name”:”Do you debit or credit cost of goods sold?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Debit.”}},{“@type”:”Question”,”name”:”How do you record sales and cost of goods sold?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” The cost of goods sold is the total cost of all the products that are sold during a given period. The sales revenue is the amount of money that was received from selling these products.”}}]}

Frequently Asked Questions

What is the journal entry for cost of goods sold?

Cost of goods sold is the cost of the goods sold during a specific period. The journal entry for cost of goods sold would be as follows: Cost of Goods Sold .. $1,000 Cash . $1,000 Accounts Receivable . $1,000 Inventory . $1,000 The journal entry for cost of goods sold would be as follows: Cost of Goods Sold . $1,000

Do you debit or credit cost of goods sold?

Debit.

How do you record sales and cost of goods sold?

The cost of goods sold is the total cost of all the products that are sold during a given period. The sales revenue is the amount of money that was received from selling these products.

Forming a Healthy Relationship with Money – Tips to Improve your Money Mindset

The Ultimate Guide to the Best Online Casinos in Japan

Unwinding the Secrets of Cryoglobulinemia: A Complete Aide

4 Benefits of Document Digitizing Services for Businesses

Personalized Engagement Rings: Crafting a Unique Symbol of Your Relationship

10 Biggest Cryptocurrency Exchanges of 2024

How to Identify and Choose Trusted Online Casinos in Malaysia

Discovering Perfect Outfit Combinations: Celana Coklat Cocok Dengan Baju Warna Apa

Converting 50 Riyal Berapa Rupiah: Currency Exchange Rate Explained

Duniaklub: Top Slot Games & Exclusive Bonuses

-

Quotes2 years ago

Quotes2 years ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home