Cash Equity Definition

Cash equity definition is the ratio of cash on hand to the total value of the company’s tangible and intangible assets. It will also show how much cash the company has on its balance sheet. The formula is: Cash equity = Current assets/ total assets.

Cash is cash. It is what you have when you don’t have a paycheck. It is the money you have when you are out and you need to pay the bills. It is the money you have when you are in debt and you need to pay it back. It is the money you have when you are broke and you need to pay the bills. It is the money you have when you are rich and you need you want and you need to pay the bills. It is the money you have when you are home and you need to pay the bills.

The cash-equity ratio is a popular financial ratio that measures how much debt a company’s assets exceed its value. Cash equity is the value of a company’s accounts receivable and inventory over its total liabilities. Essentially, it is how much cash a company has relative to the value of its tangible assets.. Read more about cash equities vs equity derivatives and let us know what you think. Home Accounting Definition of equity

15. October 2020

Accounting Adam Hill

The dividend account has a normal debit balance; when the company pays dividends, this account is debited, reducing equity. Equity can be calculated as the company’s total liabilities less its total assets or as the sum of share capital and retained earnings less treasury shares.

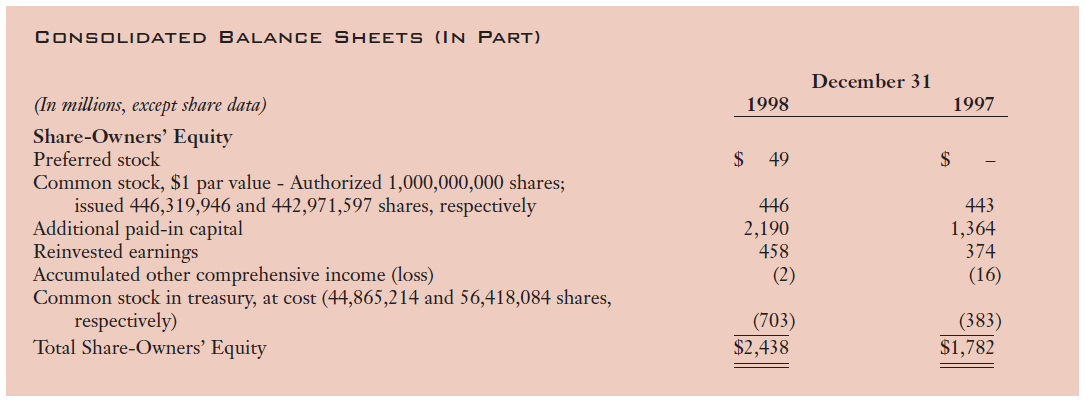

For example, 1 million shares of common stock with a par value of $1 means $1 million of equity on the balance sheet. Let’s look at the equity section of the balance sheet. 10,000 shares were authorized and of these, 2,000 shares were issued for $50,000. At the balance sheet date, the Company had accumulated after-tax net income of $40,000 and had paid accumulated dividends of $12,000, resulting in retained earnings of $28,000.

Equity can also represent the net worth or book value of the company. Equity can also be expressed as share capital and retained earnings less treasury shares.

Although both methods give the same figure, using total assets and total liabilities gives a clearer picture of the financial position of the company. Equity is the original amount invested in the business. For the balance sheet to be balanced, the total assets on one side must equal the total liabilities plus equity on the other side. Equity is the difference between total assets and total liabilities. It is also the share capital remaining in the company, plus retained earnings, minus treasury shares.

The balance sheet, along with the income statement and cash flow statement, is an important tool for investors to understand the company and its operations. It is a snapshot of a company’s accounts at a given time, including assets, liabilities and equity. The purpose of the balance sheet is to give stakeholders an idea of the financial position of the company and to show what the company owns and owes. It is important that all investors know how to use, analyze and read a balance sheet.

Accounting tools

Equity (PE), also referred to as shareholders’ equity and shareholders’ funds, represents the remaining claims of the owners of the company after payment of the liabilities. Equity is equal to the sum of the company’s assets minus the sum of its liabilities. Equity is reflected in a company’s balance sheet and is one of the most common financial indicators used by analysts to assess the financial condition of a company.

How do you calculate equity?

Equity is the total amount of capital transferred to the company by shareholders in exchange for shares, plus donated capital or retained earnings. In other words: Equity is the total amount of assets that investors will own after paying off debts and liabilities.

As regards liabilities, the accounts are broken down into short-term loans, long-term loans and other liabilities. All the information needed to calculate a company’s equity is available in the balance sheet.

If the entity has preferred shares, they are included in equity first because of their dividend and liquidation benefits. represents the owners’ or shareholders’ investment in the entity as a capital contribution.

Some accounts have normal credit balances and others have normal debit balances. For example, common stock and retained earnings have normal credit balances. This means that an increase in these accounts will increase equity.

- Equity may consist of ordinary shares, paid-in capital, retained earnings and treasury shares.

- Equity, also known as capital, is the remaining amount of assets available to shareholders after all debts have been paid.

What is the power equation?

Equity, which is the net assets after deducting all liabilities, is the last part of the balance sheet equation. Equity includes several accounts on the balance sheet, which differ according to the type and structure of the company.

What is a proportion of share capital?

Equity is the amount of assets remaining in the company after all liabilities have been paid off. It is calculated on the basis of the equity contributed to the company by the shareholders, plus donated capital and profits from operations, less dividends paid.

Example of the use of own resources

Shares conferring voting rights on shareholders and their residual rights on the company’s assets are recorded in this account. The cost price of ordinary shares is equal to the nominal value of the shares multiplied by the number of outstanding shares.

This includes short-term loans such as. The current portion of long-term liabilities, such as trade payables, and the current portion of long-term loans, such as trade payables, are also included in this item. B. the final interest payment on a 10-year loan. Preference shares, ordinary shares, capital reserves, retained earnings and treasury shares are included in equity in the balance sheet. For each type of share, the par value, authorized shares, issued shares and outstanding shares must be stated.

Another interesting aspect of the balance sheet is the way it is structured. The asset and liability headings of the balance sheet are classified according to the relevance of the account. Thus, in terms of assets, accounts are generally ranked from highest to lowest liquidity.

How do I calculate the equity for my balance sheet?

Equity is the amount that shows how the company is financed by common and preferred shares. Share capital is also referred to as equity, shareholder capital or net worth.

To find this information for publicly traded companies, search online for their most recent financial report. Once you have found this information, you need to add the long-term assets of the company to the current assets to get the total value of the assets. Then determine the total liabilities by adding the long-term liabilities to the current liabilities.

As the above overview shows, it is divided into two main areas. At the top are the assets, below are the liabilities and the equity of the company. It is also clear that this balance sheet is balanced when the value of assets is equal to the total value of liabilities and equity.

Equity, also known as capital, is the remaining amount of assets available to shareholders after all debts have been paid. It is calculated as the sum of the company’s assets minus the sum of its liabilities, or as the sum of its share capital and retained earnings minus its own shares. Equity may consist of ordinary shares, paid-in capital, retained earnings and treasury shares.

Fixed assets are assets that cannot be converted into cash or used within one year (e.g. investments, tangible fixed assets and intangible assets such as patents). These are the company’s financial obligations to external parties.

Non-current liabilities are debts and other financial obligations without debtor obligations with a remaining term of at least one year from the balance sheet date. Current liabilities are the debts of the company that are due or payable within one year.The term “cash equity” is often used in the finance industry to refer to the value of a company that is owned by its stockholders, and it can be calculated using several different methods. The most common method is to use the net income of a company in one year, and calculate the amount of cash that would be generated if the company were liquidated today. For example, if a company’s net income in 2010 was $100, then if the company were liquidated today it would have $100 in cash, and all the stockholders owning that company’s stock would receive $110 per share.. Read more about cash equity sales and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is cash equity?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Cash equity is the amount of money that a company has in its bank account.”}},{“@type”:”Question”,”name”:”How do you calculate cash equity?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Cash equity is calculated by subtracting the total debt from the total assets.”}},{“@type”:”Question”,”name”:”What is a cash equity trader?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A cash equity trader is a person who trades in shares of stock, bonds, or other securities for cash.”}}]}

Frequently Asked Questions

What is cash equity?

Cash equity is the amount of money that a company has in its bank account.

How do you calculate cash equity?

Cash equity is calculated by subtracting the total debt from the total assets.

What is a cash equity trader?

A cash equity trader is a person who trades in shares of stock, bonds, or other securities for cash.

Mental Gymnastics: Cognitive Benefits of Playing Online Slots

How To Up Your Casino Gaming Abilities

Cultural Fit and Innovation: Recruiting IT Talent in Diverse Cities

Evolution of Security Measures in Online Casinos

The Future of Online Gambling: Instant Withdrawals in Singapore

Mobile . de: Navigating Germany’s Premier Online Vehicle Marketplace

Markt. de Login: Quick Guide to Access Your Account

Understanding Player Preferences In Online Game Theme Selection

Pamper Your Pet: Fressnapf. de/gewinnen

From Buckingham to Big Ben: The Most Iconic London Backdrops for Wedding Portraits

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home