Capital Expenditure

Have you ever heard of a capital expenditure? It’s a fancy term for a business expenditure. If you’ve ever heard of a capitalized investment, you’re probably already familiar with the term. The difference between the two terms is fairly simple: capitalized investments are fixed assets you’ve purchased for very long periods of time. You can’t exactly turn around and use those assets as a capital expenditure because they’re already yours. When buying a new piece of equipment, for example, you’re not buying a capital expenditure; you’re buying a capitalized investment.

If you’ve ever noticed, all politicians seem to love spending money. They’ll talk about the need for a new hospital, or new schools, or new roads and bridges. This is all well and good, but you know where the money has to come from, right? From taxes. Now, all tax revenues come from the same place, but the government has a number of different ways to collect them, depending on what it is they’re after. So, before you go out and buy a new car, or build a new house, or fund a stadium, you should be aware of how you’ll pay for it.

On July 20, the US House of Representatives passed a bill that allows tax-free repatriation of $2.6 trillion held overseas. This repatriation provision, known as Section 965, allows US corporations to bring offshore profits back to the US without paying a tax. The bill will now be sent to President Trump for his signature, which he is expected to do.. Read more about capital expenditure meaning and let us know what you think. Fund management Investments

June 5, 2020

Accounting Adam Hill

Capital expenditure (CAPEX) is money that companies use to buy, improve or extend the life of an asset. The purpose of investments is to invest in the long-term financial health of the company. The investments are long-term investments, meaning that the acquired assets have a useful life of one year or more.

What are examples of a cost of capital?

The capital expenditure account measures a company’s total expenditure on assets over a given period and is calculated by adding the net increase in the value of the company’s tangible capital assets during the year to the depreciation expense over the same period.

How to calculate the cost of capital

When an entity makes a purchase, it may be difficult to determine whether the purchase is an asset or an expense. To simplify the decision, GAAP requires acquisitions to have an expected useful life of more than one year to be considered a capital expenditure. A recurring accounting question for every company is whether certain costs incurred should be capitalised or charged to the profit and loss account. Costs charged to the budget in a particular month shall be shown in the financial report simply as costs incurred in that month. However, capitalized costs are amortized over several years.

Most normal selling expenses are either expensed or capitalized, but some expenses may be recorded in both ways, depending on the company’s preference. Any capitalised interest is also accrued over the life of the asset. If an entity needs to apply for a line of credit to create another asset, it may capitalise the related interest expense.

Whether investments have a direct effect on profit or loss

In accounting, the investment is added to the asset account, increasing the basis (the cost or value of the asset, adjusted for tax purposes). Investments are usually presented in the cash flow statement as investments in property, plant and equipment or a similar sub-item of investments. Investments are negative because they are amounts deducted from the balance sheet or represent negative investments in the statement of cash flows. Capital expenditure, also known as investment expenditure, is used to purchase assets that will be used for your business for more than one year.

How to calculate the cost of capital

- Investments are funds used for the acquisition or modernization of fixed assets of an enterprise, such as. B. Expenditure on tangible fixed assets.

The money can also be used to improve an existing facility and extend its useful life. Examples are the expansion of an office complex, the upgrade of equipment in a factory or the installation of a wireless Internet connection in a rental property. Money spent on repairs and maintenance is not a capital expense and can be written off as a business expense in the year it is paid. Capital expenditures determine the amount a business invests in existing and new fixed assets to maintain or expand the business.

Accounting rules impose different conditions for the capitalisation of interest charges. Entities can activate interest if they create the asset themselves; they cannot activate interest on an advance to buy the asset or to pay someone else to develop it. Companies can simply think of interest expense as the cost of developing an asset. Capital expenditure – Capital expenditure is not fully expensed in the period in which it is incurred.

Expenditures for items such as equipment with a useful life of less than one year should be included in the income statement, as recommended by the IRS. A capital expenditure is an acquisition that an entity recognizes as an asset, for example. B. Property, Plant and Equipment.

The amount of the Company’s capital expenditures depends on the industry in which it operates. The Company’s purchases of property, plant and equipment, including software for internal use and website development, effectively represent its capital expenditures for the periods indicated. In the statement of cash flows, these investments appear as negative numbers (cash outflows), so the company invested $11,955 million in 2017.

Investments are funds used for the acquisition or modernization of fixed assets of an enterprise, such as. B. Expenditure on tangible fixed assets. If capital expenditures constitute a significant financial decision for the company, they must be formalized at the annual meeting or a special meeting of the board of directors.

Find the balance of the fixed asset item (PPE) on the current period balance sheet. The Company’s investments are primarily included in the fixed assets segment of the Company’s balance sheet. In addition, the amount of cash outflows incurred by the Company for capital expenditures is included in cash flows from investing activities in the statement of cash flows.

In addition to analyzing a firm’s investment in fixed assets, CapEx is used in various metrics to analyze a firm. The cash flow to capital expenditure ratio, or CF/CapEX, refers to a firm’s ability to acquire long-term assets with free cash flow. The ratio of cash flow to capital expenditures often fluctuates as companies go through cycles of large and small investments. Operating expenses are shorter-term costs that are required to cover the ongoing operating expenses of the business. Unlike capital expenditures, a company’s operating expenses are fully tax deductible in the year in which they are incurred.

Capital expenditure account

Generally accepted accounting principles (GAAP) provide guidance to companies on how to account for the initial acquisition and subsequent expenditure of assets. You can also calculate capital expenditures using data from the company’s income statement and balance sheet. In the income statement, determine the amount of depreciation expense for the current period.

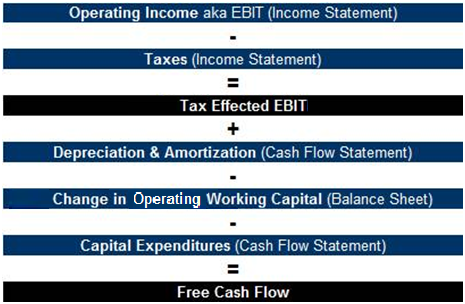

What formula is used to calculate free cash flow?

In other words: They are not fully deducted from income when calculating the company’s profit or loss. However, intangible assets are depreciated over their useful lives, while tangible assets are depreciated over their useful lives. All funds spent on the acquisition of new inventory, including equipment or intellectual property, are included in capital expenditures.

Investments can be found in the cash flow from investing activities in the company’s statement of cash flows. Not all companies identify capital expenditures in the same way. An analyst or investor might see them listed as capital expenditures, fixed asset purchases (FAPs), acquisition costs, etc.In this post I want to talk about the process of a company’s capital expenditure (i.e., investment) in the context of a business plan and how that process should be done.. Read more about capital expenditure formula and let us know what you think.{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is capital expenditure with example?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Capital expenditure is the purchase of assets that are expected to generate future benefits.”}},{“@type”:”Question”,”name”:”What is considered a capital expenditure?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” A capital expenditure is an expense that is incurred to purchase or construct a long-term asset.”}},{“@type”:”Question”,”name”:”What is capital expenditure give two examples?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:” Capital expenditure is the purchase of assets that are expected to generate future benefits. Examples of capital expenditure include the purchase of a new building, machinery, or equipment.”}}]}

Frequently Asked Questions

What is capital expenditure with example?

Capital expenditure is the purchase of assets that are expected to generate future benefits.

What is considered a capital expenditure?

A capital expenditure is an expense that is incurred to purchase or construct a long-term asset.

What is capital expenditure give two examples?

Capital expenditure is the purchase of assets that are expected to generate future benefits. Examples of capital expenditure include the purchase of a new building, machinery, or equipment.

The Biggest Mobile Game Development Trends in the Casino Sector of 2024

Immersion is the Ultimate Goal of Gaming Platforms

Boosting Solar Business Efficiency and Customer Satisfaction with FSM

Possible Risks of Shrooms Online Purchase

Silk Bonnets and LED Panels for Skin Health and Sleep Quality

How Barcode Technology Improves Emergency Room Operations

Still Thinking About Rome? How to Immerse Yourself in this Idealised Period of History

BetterThisWorld com: Unveiling New Perspectives

The Benefits of a D3K2 Supplement: Unlocking the Power of Vitamins D3 and K2

BetterThisWorld.com: Revolutionizing Social Impact Online

-

Quotes1 year ago

Quotes1 year ago30 Inspirational Thoughts For The Day

-

Self Improvement1 year ago

7 Tips To Recreate Your Life In 3 Months And Change Your Destiny

-

Motivation1 year ago

5 Excellent Ways To Stay Focused On Your Dreams

-

Quotes1 year ago

21 Quotes About Chasing Perfection And Striving For It

-

Health1 year ago

4 CBD Products Your Dog Deserves To Have

-

Personal Finance2 months ago

How Do I Find My UCAS ID Number?

-

Entrepreneurs1 year ago

1Password Evaluation – The Highest Ranked Password Manager Out There

-

Entrepreneurs2 years ago

51 Lucrative Ways to Make Money From Home